This site contains affiliate links to products. We may receive a commission for purchases made through these links, at no additional cost to you. As an Amazon Associate I earn from qualifying purchases. Read our disclaimers page for more information.

If you’re feeling overwhelmed by your debt, I get it.

After graduating college with over $30,000 in student loans (plus a maxed out credit card), I’ve felt the crushing weight of debt, too.

All of that changed when I got serious about my finances- I started with the credit card first, and was able to pay that off in about 6 months.

I took what I learned from that experience and ended up paying off a $12,000 student loan in just 3 MONTHS.

I’m fast on my way to being debt-free before I’m 30, and I’m so glad I started this journey when I did!

If you want to start your own debt-free journey, trust me when I say you CAN start now- and believe me wholeheartedly when I say you’ll be thrilled that you started!

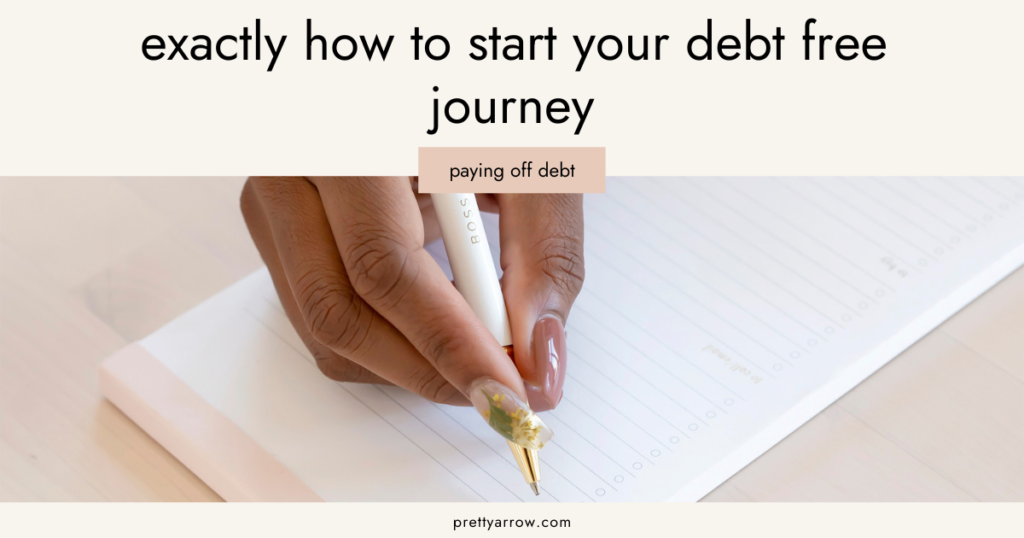

Pull out a pen and paper and let’s start your journey together!

List all of your debts in one place

The first step in any debt-payoff plan needs to be figuring out how much you owe.

Make a list of every student loan, credit card, line of credit, car loan, personal loan, etc. that you have.

You’ll want to find out the balance owing, minimum monthly payment, and interest rate for each one- this will be important later.

Stop using credit cards

This is a hard one, but it will get you far in your journey.

In order to get out of debt, you need to stop getting further into it.

If you use your cards regularly, it’s time to break up with them. Cut them up or just take them out of your wallet for a while.

Not only will this help you to get debt-free faster, but it’s also a critical step in changing your spending behaviour for good (for the better, of course!).

Change Your spending mindset

Once you have committed to hit the brakes on credit card spending, let’s talk about your spending habits.

Ask yourself: when you see something you want to buy, but you don’t have the money for it right this second- what do you do?

If you’re like a lot of others (or past me!), you use your credit card.

Without realizing it, you may be setting yourself for failure with this behaviour.

Let’s replace it with a new habit that won’t put you in debt- and still lets you buy the things you want!

Of course, taking a break from spending money entirely is the best for your bank account. However, this approach doesn’t work for everyone.

If you want to take a break from spending, start a no-spend challenge for 30 days– don’t spend money on anything except the necessities for 30 days.

If you worry this isn’t possible for you, this DOES NOT mean you will fail at your debt-free journey. Another solution is to re-think how you spend your money.

Here’s how it goes: you see something you want to buy, you add it to your shopping wish list (a list of items you want to buy and their prices), and you save up the money for it- then you buy it. This is effective because you’re not denying yourself, and you will think twice before adding the item to your wish list. Is it something you actually want to save up the money for?

Start an emergency fund

An emergency fund is a savings account that you use only for emergencies, like losing your job.

You should save 3-6 months worth of living expenses in your emergency fund.

In order to start your debt-free journey as soon as possible, you can also save up a smaller amount for now- and then add more to it once you’re debt-free.

Having even a small emergency fund while you’re committed to paying down debt is so important. When an emergency comes up, you won’t be thrown off by it. You’ll simply use your savings to cover the expense, and continue on with your plan.

Another benefit of an emergency fund is that it teaches you to rely on your own money to cover unexpected expenses that pop up, and not a credit card. Having to reach for a card when something happens would only slow down your debt payoff.

Find out how much you can afford to pay off each month

Making a budget is oh-so-important, but it becomes especially important when you’re working towards a financial goal.

A budget is not something that needs to be followed to a tee to be effective. You simply need to use it to be aware of your spending, and to get a feel for how much leftover money you have to work with each month.

List your monthly income sources, and then subtract all of your monthly expenses.

How much do you think you’ll have to add to your minimum debt payments? Keep this amount in mind.

You will continue to make the minimum payment on all of your debts, but you will focus on one at a time to pay more on (more than just the minimum payment).

Take a closer look at your monthly expenses

When is the last time you reviewed all of your monthly costs, and decided which ones could be removed or cut out entirely?

Do an audit of your monthly expenses by listing each one, and first deciding if that expense is necessary.

Could you get rid of it even just until you’re debt-free? Is it something you forgot you were paying for, and should cut out for good?

Some expenses, like groceries and transportation, are always necessary- but they can be reduced, giving you more money to put towards your debt!

Some recurring bills, like your phone bill, can also be reduced by negotiating with your phone provider or by changing to a cheaper plan.

When I committed to paying off my student loans, I went with a cheaper phone and internet bill- plus I moved to a cheaper apartment. I found a few subscriptions that I forgot I was paying for, too. To cut down on miscellaneous spending, I also committed to buying second-hand goods only until I was debt-free.

Make sure that you take the time to carefully assess each of your bills- you may be surprised how much you can save yourself!

If you want to review your spending the easy way, check out Trim!

Trim is an app that constantly works to help save you money. Here’s how it works: once you link your credit or debit card, Trim helps you to cancel old subscriptions, set spending alerts, check how much you’re spending in certain areas, and automatically fight fees. They can even negotiate your monthly bill costs for you! Sign up for Trim here!

Pick a Debt Repayment Method- Snowball or Avalanche?

Now that you know how much extra money you have to put towards your debt each month, how do you know where to allocate that money? Do you divide it up equally amongst several credit cards or loans?

There are two debt repayment methods that could work well for you- these methods are so helpful because they were designed to keep you motivated along the way!

Note that you will continue to make the minimum payments on all of your debts- these repayment methods will help you to determine which debt you will pay more on (above and beyond the minimum payment).

The Debt Avalanche method is where you pay off your debts in order from the highest to the lowest interest rate.

If it drives you crazy how much you’re paying in interest, then paying off the highest interest rate first should keep you motivated.

Once you have the first debt paid off, move on to the debt with the next highest interest rate- start to put extra money on this debt every month now (including the payment from the debt that’s now been paid off). Repeat until you are debt-free!

The Debt Snowball method is similar, except you’re paying your debts off in order from the lowest amount owing to the highest. This is how I have been paying off my debt. By starting with the smaller debts, they will take less time to be paid off.

Even if it’s a small debt, you’ll feel great when one is paid off! You’ll feel motivated to stick to it as each debt is eliminated.

Bonus Tip: Start a side hustle to get out of debt

If you’re in the business of getting out of debt fast, you’re already on the right track.

You’ve stopped using your credit cards, you’ve reduced your monthly expenses as much as you can, and you’re putting more money on your debt than ever before.

At the end of the day, there’s only so many expenses you can cut out. Want to throw even more money at your debt every month? Start a side hustle!

This could be starting your own business (like a blog!) to make extra cash, or it can be a part-time job.

If you’re not sure if it’s worth it, figure out how much money you could make at a part-time job in your area. Would you be looking at another $100, $200, or $500 a month?

If you had an extra $500 a month to pay off your debt, how quickly could you be debt-free?

This may or may not be worth it for you, but oftentimes, this is a sure-fire way to get out of debt quicker than you would by just cutting costs every month.

Becoming debt-free is no small task, but the reward at the end is a big one!

Imagine what you can do with your money when you don’t have monthly payments to make on student loans or credit cards. That’s exactly what is pushing me to get rid of debt for good, and I can’t wait to get there!

What is driving you to pay off your debt? Share your debt-free motivation below!

Howdy just wanted to give you a quick heads up. The text in your post seem to be running off the screen in Chrome. I’m not sure if this is a formatting issue or something to do with browser compatibility but I figured I’d post to let you know. The layout look great though! Hope you get the issue resolved soon. Thanks

Saved as a favorite, I really like your blog!

I haven¦t checked in here for a while as I thought it was getting boring, but the last few posts are good quality so I guess I will add you back to my everyday bloglist. You deserve it my friend 🙂

Great article and right to the point. I don’t know if this is in fact the best place to ask but do you guys have any thoughts on where to hire some professional writers? Thanks in advance 🙂

Nice post. I learn something more challenging on different blogs everyday. It will always be stimulating to read content from other writers and practice a little something from their store. I’d prefer to use some with the content on my blog whether you don’t mind. Natually I’ll give you a link on your web blog. Thanks for sharing.

You have brought up a very excellent details, regards for the post.

Woah! I’m really digging the template/theme of this blog. It’s simple, yet effective. A lot of times it’s difficult to get that “perfect balance” between usability and appearance. I must say you have done a amazing job with this. Also, the blog loads extremely fast for me on Opera. Superb Blog!

Good write-up, I¦m regular visitor of one¦s web site, maintain up the excellent operate, and It’s going to be a regular visitor for a long time.

You made some good points there. I looked on the internet for the subject and found most persons will approve with your site.

Greetings from Carolina! I’m bored to death at work so I decided to browse your site on my iphone during lunch break. I really like the information you provide here and can’t wait to take a look when I get home. I’m shocked at how quick your blog loaded on my phone .. I’m not even using WIFI, just 3G .. Anyhow, awesome site!

It’s a shame you don’t have a donate button! I’d without a doubt donate to this brilliant blog! I suppose for now i’ll settle for book-marking and adding your RSS feed to my Google account. I look forward to brand new updates and will talk about this site with my Facebook group. Chat soon!

Appreciating the time and energy you put into your website and in depth information you provide. It’s good to come across a blog every once in a while that isn’t the same out of date rehashed information. Great read! I’ve bookmarked your site and I’m adding your RSS feeds to my Google account.

Excellent goods from you, man. I’ve understand your stuff previous to and you’re just too magnificent. I actually like what you have acquired here, certainly like what you are stating and the way in which you say it. You make it enjoyable and you still take care of to keep it smart. I can not wait to read far more from you. This is really a wonderful site.

Wonderful goods from you, man. I have understand your stuff previous to and you are just extremely magnificent. I actually like what you have acquired here, really like what you’re saying and the way in which you say it. You make it entertaining and you still take care of to keep it sensible. I cant wait to read much more from you. This is actually a great website.

I have been browsing online greater than 3 hours these days, but I never discovered any interesting article like yours. It’s lovely worth enough for me. Personally, if all website owners and bloggers made good content material as you probably did, the net shall be a lot more useful than ever before.

This design is spectacular! You most certainly know how to keep a reader amused. Between your wit and your videos, I was almost moved to start my own blog (well, almost…HaHa!) Fantastic job. I really enjoyed what you had to say, and more than that, how you presented it. Too cool!

Thanks for the article, is there any way I can receive an alert email every time there is a fresh post?

Hey there, You’ve done an incredible job. I will certainly digg it and personally recommend to my friends. I’m confident they will be benefited from this website.

Thanks for sharing excellent informations. Your web-site is very cool. I am impressed by the details that you’ve on this website. It reveals how nicely you understand this subject. Bookmarked this web page, will come back for more articles. You, my pal, ROCK! I found just the info I already searched all over the place and just could not come across. What a great website.

This website is my intake, real wonderful design and perfect subject material.

This design is wicked! You obviously know how to keep a reader entertained. Between your wit and your videos, I was almost moved to start my own blog (well, almost…HaHa!) Fantastic job. I really enjoyed what you had to say, and more than that, how you presented it. Too cool!

Very clean internet site, regards for this post.

I have been exploring for a little for any high quality articles or weblog posts on this sort of space . Exploring in Yahoo I ultimately stumbled upon this website. Reading this info So i am happy to express that I’ve an incredibly just right uncanny feeling I discovered exactly what I needed. I so much certainly will make certain to do not put out of your mind this site and give it a look regularly.

I like this weblog very much so much good info .

Oh my goodness! a tremendous article dude. Thank you Nevertheless I am experiencing difficulty with ur rss . Don’t know why Unable to subscribe to it. Is there anyone getting similar rss drawback? Anybody who is aware of kindly respond. Thnkx

I¦ll right away grab your rss feed as I can’t find your e-mail subscription hyperlink or e-newsletter service. Do you have any? Please let me recognize in order that I may subscribe. Thanks.

An interesting discussion is worth comment. I think that you should write more on this topic, it might not be a taboo subject but generally people are not enough to speak on such topics. To the next. Cheers

you are really a good webmaster. The site loading speed is incredible. It seems that you are doing any unique trick. In addition, The contents are masterwork. you have done a fantastic job on this topic!

Thanks for helping out, great info .

Somebody essentially help to make seriously articles I would state. This is the first time I frequented your website page and thus far? I surprised with the research you made to create this particular publish incredible. Fantastic job!

Thanks for another informative blog. Where else could I get that kind of info written in such an ideal way? I’ve a project that I’m just now working on, and I’ve been on the look out for such information.

Thank you, I’ve just been looking for information approximately this topic for ages and yours is the greatest I’ve found out till now. However, what in regards to the conclusion? Are you positive in regards to the supply?

Thank you for every other informative site. The place else may I am getting that type of info written in such a perfect approach? I’ve a mission that I am just now operating on, and I have been on the glance out for such information.

It is in reality a great and useful piece of info. I¦m satisfied that you just shared this useful information with us. Please keep us up to date like this. Thanks for sharing.

I reckon something truly special in this web site.

Hello there! This post couldn’t be written any better! Reading this post reminds me of my good old room mate! He always kept chatting about this. I will forward this page to him. Pretty sure he will have a good read. Thank you for sharing!

What i do not realize is actually how you’re not really much more smartly-preferred than you may be right now. You are very intelligent. You understand therefore significantly in terms of this subject, made me in my opinion consider it from so many numerous angles. Its like women and men aren’t interested except it?¦s something to accomplish with Girl gaga! Your individual stuffs nice. At all times take care of it up!

Hello very cool blog!! Guy .. Beautiful .. Wonderful .. I will bookmark your site and take the feeds additionally…I am glad to find numerous useful information here within the post, we want develop more strategies in this regard, thanks for sharing.

I am extremely impressed with your writing skills and also with the layout on your weblog. Is this a paid theme or did you modify it yourself? Anyway keep up the nice quality writing, it is rare to see a nice blog like this one nowadays..

Good day very cool site!! Man .. Beautiful .. Wonderful .. I will bookmark your website and take the feeds additionallyKI’m happy to find a lot of helpful info here in the publish, we want develop more strategies in this regard, thank you for sharing. . . . . .

You have brought up a very fantastic points, regards for the post.

Thanks for the sensible critique. Me & my neighbor were just preparing to do some research on this. We got a grab a book from our local library but I think I learned more from this post. I’m very glad to see such wonderful info being shared freely out there.

I’ll right away grab your rss feed as I can’t find your email subscription link or newsletter service. Do you have any? Please let me know in order that I could subscribe. Thanks.

Hi there! I know this is kinda off topic but I’d figured I’d ask. Would you be interested in exchanging links or maybe guest authoring a blog article or vice-versa? My blog covers a lot of the same topics as yours and I believe we could greatly benefit from each other. If you happen to be interested feel free to send me an email. I look forward to hearing from you! Terrific blog by the way!

I know this if off topic but I’m looking into starting my own blog and was wondering what all is needed to get setup? I’m assuming having a blog like yours would cost a pretty penny? I’m not very internet savvy so I’m not 100 certain. Any suggestions or advice would be greatly appreciated. Thank you

F*ckin’ tremendous things here. I’m very happy to look your article. Thanks a lot and i am having a look ahead to contact you. Will you please drop me a mail?

Hello! This is kind of off topic but I need some help from an established blog. Is it tough to set up your own blog? I’m not very techincal but I can figure things out pretty quick. I’m thinking about creating my own but I’m not sure where to begin. Do you have any ideas or suggestions? With thanks

Good info. Lucky me I reach on your website by accident, I bookmarked it.

Hi, Neat post. There is a problem along with your site in web explorer, would check this… IE nonetheless is the marketplace leader and a huge component to people will omit your great writing due to this problem.

Attractive section of content. I just stumbled upon your blog and in accession capital to assert that I get actually enjoyed account your blog posts. Any way I will be subscribing to your feeds and even I achievement you access consistently rapidly.

Very interesting subject, thank you for putting up.

I went over this web site and I believe you have a lot of great info , saved to favorites (:.

You should take part in a contest for probably the greatest blogs on the web. I’ll advocate this web site!

Good web site! I really love how it is simple on my eyes and the data are well written. I am wondering how I might be notified whenever a new post has been made. I have subscribed to your feed which must do the trick! Have a great day!

naturally like your web-site but you have to check the spelling on several of your posts. A number of them are rife with spelling problems and I find it very troublesome to tell the truth nevertheless I’ll certainly come back again.

Have you ever considered about including a little bit more than just your articles? I mean, what you say is important and everything. Nevertheless just imagine if you added some great visuals or videos to give your posts more, “pop”! Your content is excellent but with pics and clips, this website could certainly be one of the very best in its field. Terrific blog!

Your house is valueble for me. Thanks!…

Thanks a bunch for sharing this with all of us you actually know what you’re talking about! Bookmarked. Please also visit my web site =). We could have a link exchange contract between us!

I like this post, enjoyed this one appreciate it for putting up.

Today, I went to the beach with my children. I found a sea shell and gave it to my 4 year old daughter and said “You can hear the ocean if you put this to your ear.” She placed the shell to her ear and screamed. There was a hermit crab inside and it pinched her ear. She never wants to go back! LoL I know this is entirely off topic but I had to tell someone!

Excellent weblog right here! Also your website lots up fast! What web host are you the use of? Can I get your affiliate hyperlink for your host? I want my web site loaded up as fast as yours lol

Thank you for the good writeup. It in fact was a amusement account it. Look advanced to more added agreeable from you! By the way, how can we communicate?

I’m not that much of a online reader to be honest but your blogs really nice, keep it up! I’ll go ahead and bookmark your website to come back later on. All the best

I know this if off topic but I’m looking into starting my own weblog and was curious what all is needed to get set up? I’m assuming having a blog like yours would cost a pretty penny? I’m not very internet savvy so I’m not 100 sure. Any recommendations or advice would be greatly appreciated. Thank you

I do agree with all the ideas you’ve presented in your post. They’re really convincing and will certainly work. Still, the posts are very short for novices. Could you please extend them a bit from next time? Thanks for the post.

Really Appreciate this post, can you make it so I receive an update sent in an email whenever there is a fresh article?

Great wordpress blog here.. It’s hard to find quality writing like yours these days. I really appreciate people like you! take care

I have been absent for a while, but now I remember why I used to love this blog. Thank you, I’ll try and check back more often. How frequently you update your web site?

great post, very informative. I wonder why the other specialists of this sector do not notice this. You must continue your writing. I’m sure, you have a huge readers’ base already!

Normally I don’t read article on blogs, but I would like to say that this write-up very forced me to try and do so! Your writing style has been amazed me. Thanks, very nice post.

I always was concerned in this subject and still am, appreciate it for putting up.

Some really interesting information, well written and generally user friendly.

I am continually browsing online for ideas that can facilitate me. Thx!

Glad to be one of many visitors on this awing internet site : D.

Have you ever thought about creating an e-book or guest authoring on other sites? I have a blog based on the same ideas you discuss and would love to have you share some stories/information. I know my visitors would appreciate your work. If you are even remotely interested, feel free to send me an e-mail.

What¦s Happening i’m new to this, I stumbled upon this I’ve found It positively useful and it has aided me out loads. I am hoping to contribute & assist different customers like its helped me. Great job.

Some really interesting info , well written and broadly speaking user genial.

I’ll right away snatch your rss feed as I can’t to find your email subscription link or newsletter service. Do you’ve any? Please allow me recognize in order that I may subscribe. Thanks.

Hey There. I found your blog using msn. This is a really well written article. I’ll make sure to bookmark it and return to read more of your useful info. Thanks for the post. I’ll definitely return.

What¦s Taking place i’m new to this, I stumbled upon this I’ve found It absolutely useful and it has helped me out loads. I’m hoping to give a contribution & aid different customers like its aided me. Great job.

Thank you for another magnificent article. Where else could anyone get that type of info in such a perfect way of writing? I’ve a presentation next week, and I’m on the look for such info.

Magnificent web site. A lot of useful info here. I’m sending it to some friends ans also sharing in delicious. And of course, thanks for your effort!

Hi! This is my first visit to your blog! We are a group of volunteers and starting a new project in a community in the same niche. Your blog provided us beneficial information to work on. You have done a extraordinary job!

Appreciate it for helping out, great info. “Riches cover a multitude of woes.” by Menander.

Thank you for sharing with us, I think this website really stands out : D.

When I originally commented I clicked the -Notify me when new comments are added- checkbox and now each time a comment is added I get four emails with the same comment. Is there any way you can remove me from that service? Thanks!

Wow, amazing weblog format! How long have you been running a blog for? you make running a blog look easy. The full look of your web site is excellent, as neatly as the content material!

I was very pleased to find this web-site.I wanted to thanks for your time for this wonderful read!! I definitely enjoying every little bit of it and I have you bookmarked to check out new stuff you blog post.

I am glad to be a visitor of this pure website! , regards for this rare info ! .

Thank you for another informative blog. Where else could I get that type of info written in such an ideal way? I have a project that I’m just now working on, and I have been on the look out for such info.

I was suggested this web site by my cousin. I am not sure whether this post is written by him as no one else know such detailed about my difficulty. You’re amazing! Thanks!

It is appropriate time to make some plans for the future and it’s time to be happy. I’ve read this submit and if I may I wish to counsel you some fascinating things or advice. Perhaps you could write subsequent articles relating to this article. I desire to read more issues about it!

Thank you so much for providing individuals with such a superb possiblity to read critical reviews from this site. It really is so enjoyable and also full of amusement for me and my office mates to search your site on the least thrice in a week to see the latest items you have. And indeed, I am usually satisfied considering the mind-blowing inspiring ideas you serve. Selected 4 ideas on this page are easily the very best we have had.

What i do not understood is actually how you are no longer actually much more well-liked than you may be now. You’re so intelligent. You recognize therefore significantly in terms of this matter, made me in my view imagine it from numerous numerous angles. Its like men and women aren’t involved except it¦s one thing to do with Girl gaga! Your individual stuffs excellent. All the time care for it up!

Simply desire to say your article is as astounding. The clarity to your publish is simply nice and i could assume you’re an expert on this subject. Well along with your permission allow me to take hold of your RSS feed to stay updated with coming near near post. Thank you a million and please continue the rewarding work.

Woah! I’m really loving the template/theme of this blog. It’s simple, yet effective. A lot of times it’s very hard to get that “perfect balance” between usability and visual appearance. I must say that you’ve done a great job with this. Additionally, the blog loads extremely fast for me on Chrome. Exceptional Blog!

Hmm is anyone else encountering problems with the images on this blog loading? I’m trying to find out if its a problem on my end or if it’s the blog. Any responses would be greatly appreciated.

Please let me know if you’re looking for a writer for your site. You have some really great articles and I think I would be a good asset. If you ever want to take some of the load off, I’d absolutely love to write some articles for your blog in exchange for a link back to mine. Please shoot me an e-mail if interested. Thanks!

I love your blog.. very nice colors & theme. Did you make this website yourself or did you hire someone to do it for you? Plz answer back as I’m looking to create my own blog and would like to find out where u got this from. thank you

Hi there! This is my first visit to your blog! We are a collection of volunteers and starting a new initiative in a community in the same niche. Your blog provided us useful information to work on. You have done a outstanding job!

great points altogether, you simply gained a new reader. What would you suggest in regards to your post that you made some days ago? Any positive?

I love how user-friendly and intuitive everything feels.

I?¦ve recently started a site, the info you provide on this website has helped me greatly. Thank you for all of your time & work.

I love how user-friendly and intuitive everything feels.

I really like your writing style, excellent information, thank you for posting :D. “Every moment of one’s existence one is growing into more or retreating into less.” by Norman Mailer.

I am glad to be one of the visitants on this outstanding website (:, regards for posting.

Hi, Neat post. There is a problem with your site in internet explorer, would test this… IE still is the market leader and a huge portion of people will miss your excellent writing because of this problem.

The layout is visually appealing and very functional.

Thank you for sharing superb informations. Your website is very cool. I am impressed by the details that you have on this blog. It reveals how nicely you perceive this subject. Bookmarked this website page, will come back for extra articles. You, my friend, ROCK! I found simply the info I already searched all over the place and simply couldn’t come across. What a perfect site.

The design and usability are top-notch, making everything flow smoothly.

Mitolyn is a cutting-edge natural dietary supplement designed to support effective weight loss and improve overall wellness.

I’m really impressed by the speed and responsiveness.

At this time it looks like Drupal is the top blogging platform available right now. (from what I’ve read) Is that what you’re using on your blog?

A perfect blend of aesthetics and functionality makes browsing a pleasure.

Mitolyn is a cutting-edge natural dietary supplement designed to support effective weight loss and improve overall wellness.

Good write-up, I am regular visitor of one¦s site, maintain up the excellent operate, and It is going to be a regular visitor for a lengthy time.

This site truly stands out as a great example of quality web design and performance.

Good – I should definitely pronounce, impressed with your site. I had no trouble navigating through all tabs as well as related information ended up being truly easy to do to access. I recently found what I hoped for before you know it at all. Quite unusual. Is likely to appreciate it for those who add forums or something, web site theme . a tones way for your client to communicate. Excellent task..

The Ice Water Hack has gained popularity as a simple yet effective method for boosting metabolism and promoting weight loss.

I’m really impressed by the speed and responsiveness.

I am glad to be one of the visitants on this great site (:, regards for posting.

The content is engaging and well-structured, keeping visitors interested.

I have been exploring for a little for any high quality articles or weblog posts on this kind of space . Exploring in Yahoo I at last stumbled upon this site. Studying this information So i am happy to express that I’ve a very good uncanny feeling I discovered just what I needed. I such a lot certainly will make sure to do not forget this web site and provides it a glance regularly.

It provides an excellent user experience from start to finish.

The content is well-organized and highly informative.

The design and usability are top-notch, making everything flow smoothly.

Very interesting points you have mentioned, thanks for posting. “I’ve made a couple of mistakes I’d like to do over.” by Jerry Coleman.

Normally I don’t learn post on blogs, however I would like to say that this write-up very compelled me to check out and do so! Your writing style has been surprised me. Thank you, very great post.

I like what you guys are up too. Such intelligent work and reporting! Carry on the superb works guys I’ve incorporated you guys to my blogroll. I think it’ll improve the value of my website 🙂

You got a very great website, Gladiola I discovered it through yahoo.

Really enjoyed this post, can I set it up so I receive an email every time you publish a new update?

Very nice design and style and good written content, nothing at all else we want : D.

very good post, i actually love this web site, keep on it

I like this blog very much so much fantastic information.

AI is evolving so fast! I can’t wait to see how it transforms our daily lives in the next decade. The possibilities are endless, from automation to medical advancements.

I couldn’t resist commenting

You are my aspiration, I possess few web logs and often run out from to brand : (.

Japan is definitely on my bucket list! The mix of tradition and modernity is fascinating, and the food alone is enough reason to visit.

Every expert was once a beginner. Keep pushing forward, and one day, you’ll look back and see how far you’ve come. Progress is always happening, even when it doesn’t feel like it.

Thanks , I’ve just been looking for info about this subject for ages and yours is the greatest I have discovered till now. But, what about the conclusion? Are you sure about the source?

I was just searching for this information for some time. After 6 hours of continuous Googleing, at last I got it in your website. I wonder what’s the lack of Google strategy that do not rank this kind of informative sites in top of the list. Normally the top sites are full of garbage.

AI is evolving so fast! I can’t wait to see how it transforms our daily lives in the next decade. The possibilities are endless, from automation to medical advancements.

Whats up very nice website!! Guy .. Beautiful .. Amazing .. I’ll bookmark your web site and take the feeds additionally…I’m glad to find so many helpful information here within the put up, we’d like develop extra techniques on this regard, thanks for sharing.

Amazing blog! Do you have any tips and hints for aspiring writers? I’m planning to start my own site soon but I’m a little lost on everything. Would you recommend starting with a free platform like WordPress or go for a paid option? There are so many choices out there that I’m completely overwhelmed .. Any tips? Thanks a lot!

Christopher Nolan’s storytelling is always mind-blowing. Every movie feels like a masterpiece, and the way he plays with time and perception is just genius.

Thanks for another great article. The place else could anybody get that type of info in such a perfect method of writing? I’ve a presentation next week, and I am on the look for such info.

so much good info on here, : D.

I want foregathering useful info, this post has got me even more info! .

Good post but I was wondering if you could write a litte more on this topic? I’d be very grateful if you could elaborate a little bit further. Thank you!

I like the valuable info you provide to your articles. I will bookmark your blog and take a look at once more here regularly. I’m reasonably sure I’ll be informed plenty of new stuff proper here! Best of luck for the following!

I like this post, enjoyed this one appreciate it for posting. “We are punished by our sins, not for them.” by Elbert Hubbard.

hello there and thank you for your info – I’ve definitely picked up something new from right here. I did however expertise some technical issues using this website, since I experienced to reload the website lots of times previous to I could get it to load properly. I had been wondering if your web hosting is OK? Not that I’m complaining, but slow loading instances times will very frequently affect your placement in google and could damage your high-quality score if ads and marketing with Adwords. Anyway I’m adding this RSS to my e-mail and could look out for a lot more of your respective intriguing content. Ensure that you update this again very soon..

Only wanna remark on few general things, The website pattern is perfect, the content material is very excellent. “War is much too serious a matter to be entrusted to the military.” by Georges Clemenceau.

hello!,I love your writing very so much! share we communicate extra approximately your post on AOL? I need an expert on this area to solve my problem. Maybe that is you! Looking forward to look you.

Woah! I’m really digging the template/theme of this site. It’s simple, yet effective. A lot of times it’s difficult to get that “perfect balance” between superb usability and appearance. I must say you have done a awesome job with this. In addition, the blog loads super fast for me on Firefox. Outstanding Blog!

Mitolyn is a cutting-edge natural dietary supplement designed to support effective weight loss and improve overall wellness.

Mitolyn is a cutting-edge natural dietary supplement designed to support effective weight loss and improve overall wellness.

Absolutely written subject matter, thank you for selective information. “He who establishes his argument by noise and command shows that his reason is weak.” by Michel de Montaigne.

When I originally commented I clicked the -Notify me when new comments are added- checkbox and now each time a comment is added I get four emails with the same comment. Is there any way you can remove me from that service? Thanks!

I dugg some of you post as I cerebrated they were very useful very beneficial

PrimeBiome is a dietary supplement designed to support gut health by promoting a balanced microbiome, enhancing digestion, and boosting overall well-being.

Thank you for sharing with us, I believe this website genuinely stands out : D.

PrimeBiome is a dietary supplement designed to support gut health by promoting a balanced microbiome, enhancing digestion, and boosting overall well-being.

I’ve recently started a website, the info you offer on this website has helped me tremendously. Thank you for all of your time & work.

Wow, wonderful blog layout! How long have you ever been blogging for? you made running a blog glance easy. The entire look of your site is magnificent, let alone the content material!

Rattling fantastic information can be found on web site. “There used to be a real me, but I had it surgically removed.” by Peter Sellers.

I’ve recently started a blog, the info you provide on this site has helped me tremendously. Thanks for all of your time & work.

I simply needed to say thanks once more. I am not sure the things that I would’ve used in the absence of those opinions shown by you concerning that concern. This has been a depressing concern in my circumstances, nevertheless considering the specialized way you handled the issue forced me to jump over contentment. I am just happier for your work and even hope that you find out what a powerful job you happen to be accomplishing training some other people all through a blog. More than likely you haven’t met any of us.

Great write-up, I am regular visitor of one¦s site, maintain up the nice operate, and It’s going to be a regular visitor for a lengthy time.

The Natural Mounjaro Recipe is more than just a diet—it’s a sustainable and natural approach to weight management and overall health.

I am constantly searching online for tips that can facilitate me. Thx!

Great – I should definitely pronounce, impressed with your website. I had no trouble navigating through all tabs as well as related info ended up being truly simple to do to access. I recently found what I hoped for before you know it at all. Quite unusual. Is likely to appreciate it for those who add forums or something, web site theme . a tones way for your customer to communicate. Nice task..

Thanks for any other wonderful post. Where else could anyone get that kind of info in such an ideal means of writing? I’ve a presentation next week, and I’m on the search for such info.

Nitric Boost Ultra is a dietary supplement designed to enhance cardiovascular health, energy levels, and endurance by increasing nitric oxide (NO) production in the body.

I’m not sure exactly why but this website is loading extremely slow for me. Is anyone else having this problem or is it a issue on my end? I’ll check back later on and see if the problem still exists.

I’ve been surfing online more than 3 hours today, yet I never found any interesting article like yours. It is pretty worth enough for me. Personally, if all website owners and bloggers made good content as you did, the internet will be much more useful than ever before.

Fantastic post however I was wondering if you could write a litte more on this subject? I’d be very grateful if you could elaborate a little bit more. Kudos!

Precisely what I was looking for, thanks for posting.

PrimeBiome is a dietary supplement designed to support gut health by promoting a balanced microbiome, enhancing digestion, and boosting overall well-being.

I like what you guys are up also. Such clever work and reporting! Carry on the superb works guys I’ve incorporated you guys to my blogroll. I think it’ll improve the value of my site 🙂

PrimeBiome is a dietary supplement designed to support gut health by promoting a balanced microbiome, enhancing digestion, and boosting overall well-being.

I savor, cause I found exactly what I used to be looking for. You have ended my 4 day lengthy hunt! God Bless you man. Have a nice day. Bye

Hmm it looks like your blog ate my first comment (it was extremely long) so I guess I’ll just sum it up what I had written and say, I’m thoroughly enjoying your blog. I as well am an aspiring blog blogger but I’m still new to everything. Do you have any points for first-time blog writers? I’d certainly appreciate it.

ProDentim is a cutting-edge oral health supplement designed to improve dental and gum health by leveraging natural probiotics and nutrientes.

The Natural Mounjaro Recipe is more than just a diet—it’s a sustainable and natural approach to weight management and overall health.

I am always thought about this, regards for posting.

There is noticeably a bunch to know about this. I think you made various nice points in features also.

Valuable information. Lucky me I found your site by accident, and I am shocked why this accident did not happened earlier! I bookmarked it.

Well I really liked studying it. This subject offered by you is very helpful for correct planning.

very nice put up, i definitely love this web site, keep on it

The next time I read a blog, I hope that it doesnt disappoint me as much as this one. I mean, I know it was my choice to read, but I actually thought youd have something interesting to say. All I hear is a bunch of whining about something that you could fix if you werent too busy looking for attention.

You actually make it seem so easy with your presentation but I find this topic to be really something that I think I would never understand. It seems too complex and very broad for me. I am looking forward for your next post, I will try to get the hang of it!

Loving the info on this web site, you have done great job on the content.

Thanks a bunch for sharing this with all of us you actually know what you’re talking about! Bookmarked. Please also visit my website =). We could have a link exchange agreement between us!

Pretty part of content. I just stumbled upon your site and in accession capital to claim that I acquire actually enjoyed account your blog posts. Anyway I will be subscribing for your feeds and even I achievement you access constantly quickly.

I wanted to thank you for this great read!! I definitely enjoying every little bit of it I have you bookmarked to check out new stuff you post…

I like the valuable information you provide in your articles. I will bookmark your weblog and check again here regularly. I am quite certain I will learn plenty of new stuff right here! Good luck for the next!

Howdy! I’m at work browsing your blog from my new iphone 3gs! Just wanted to say I love reading your blog and look forward to all your posts! Keep up the superb work!

I have been exploring for a little bit for any high-quality articles or blog posts on this sort of area . Exploring in Yahoo I eventually stumbled upon this site. Reading this information So i’m satisfied to convey that I have a very good uncanny feeling I found out just what I needed. I such a lot definitely will make certain to do not forget this site and provides it a glance on a relentless basis.

I got what you mean , regards for posting.Woh I am lucky to find this website through google. “Spare no expense to make everything as economical as possible.” by Samuel Goldwyn.

Very interesting information!Perfect just what I was looking for! “Wherever the Turkish hoof trods, no grass grows.” by Victor Hugo.

Magnificent beat ! I would like to apprentice whilst you amend your web site, how could i subscribe for a weblog site? The account helped me a applicable deal. I had been tiny bit familiar of this your broadcast offered vivid transparent idea

I really appreciate this post. I have been looking everywhere for this! Thank goodness I found it on Bing. You’ve made my day! Thx again!

I’ll right away grab your rss as I can’t find your email subscription link or e-newsletter service. Do you have any? Kindly let me realize so that I may just subscribe. Thanks.

Well I really liked studying it. This post offered by you is very effective for good planning.

I’d have to examine with you here. Which is not one thing I usually do! I take pleasure in reading a post that may make folks think. Additionally, thanks for permitting me to comment!

Appreciate it for this marvelous post, I am glad I noticed this website on yahoo.

Hey there! I know this is kinda off topic nevertheless I’d figured I’d ask. Would you be interested in exchanging links or maybe guest authoring a blog article or vice-versa? My site goes over a lot of the same topics as yours and I feel we could greatly benefit from each other. If you’re interested feel free to shoot me an email. I look forward to hearing from you! Awesome blog by the way!

Pretty! This was a really wonderful post. Thank you for your provided information.

I got what you intend, appreciate it for putting up.Woh I am glad to find this website through google.

If everything in this universe has a cause, then surely the cause of my hunger must be the divine order of things aligning to guide me toward the ultimate pleasure of a well-timed meal. Could it be that desire itself is a cosmic signal, a way for nature to communicate with us, pushing us toward the fulfillment of our potential? Perhaps the true philosopher is not the one who ignores his desires, but the one who understands their deeper meaning.

Even the gods, if they exist, must laugh from time to time. Perhaps what we call tragedy is merely comedy from a higher perspective, a joke we are too caught up in to understand. Maybe the wisest among us are not the ones who take life the most seriously, but those who can laugh at its absurdity and find joy even in the darkest moments.

Good day! This is kind of off topic but I need some advice from an established blog. Is it hard to set up your own blog? I’m not very techincal but I can figure things out pretty quick. I’m thinking about making my own but I’m not sure where to begin. Do you have any ideas or suggestions? Thank you

The potential within all things is a mystery that fascinates me endlessly. A tiny seed already contains within it the entire blueprint of a towering tree, waiting for the right moment to emerge. Does the seed know what it will become? Do we? Or are we all simply waiting for the right conditions to awaken into what we have always been destined to be?

I just like the helpful information you provide on your articles. I will bookmark your weblog and take a look at again right here regularly. I’m reasonably sure I will be informed many new stuff right right here! Good luck for the following!

Somebody essentially help to make seriously posts I would state. This is the very first time I frequented your website page and thus far? I surprised with the research you made to make this particular publish extraordinary. Excellent job!

Some truly interesting points you have written.Assisted me a lot, just what I was searching for : D.

he blog was how do i say it… relevant, finally something that helped me. Thanks

If everything in this universe has a cause, then surely the cause of my hunger must be the divine order of things aligning to guide me toward the ultimate pleasure of a well-timed meal. Could it be that desire itself is a cosmic signal, a way for nature to communicate with us, pushing us toward the fulfillment of our potential? Perhaps the true philosopher is not the one who ignores his desires, but the one who understands their deeper meaning.

You are a very intelligent individual!

Friendship, some say, is a single soul residing in two bodies, but why limit it to two? What if friendship is more like a great, endless web, where each connection strengthens the whole? Maybe we are not separate beings at all, but parts of one vast consciousness, reaching out through the illusion of individuality to recognize itself in another.

The essence of existence is like smoke, always shifting, always changing, yet somehow always present. It moves with the wind of thought, expanding and contracting, never quite settling but never truly disappearing. Perhaps to exist is simply to flow, to let oneself be carried by the great current of being without resistance.

I like examining and I conceive this website got some genuinely utilitarian stuff on it! .

I am forever thought about this, appreciate it for putting up.

Please let me know if you’re looking for a article author for your blog. You have some really good articles and I think I would be a good asset. If you ever want to take some of the load off, I’d really like to write some material for your blog in exchange for a link back to mine. Please blast me an email if interested. Regards!

The essence of existence is like smoke, always shifting, always changing, yet somehow always present. It moves with the wind of thought, expanding and contracting, never quite settling but never truly disappearing. Perhaps to exist is simply to flow, to let oneself be carried by the great current of being without resistance.

I am perpetually thought about this, thanks for putting up.

Woah! I’m really loving the template/theme of this website. It’s simple, yet effective. A lot of times it’s hard to get that “perfect balance” between user friendliness and appearance. I must say that you’ve done a fantastic job with this. In addition, the blog loads very fast for me on Safari. Exceptional Blog!

Whats Taking place i am new to this, I stumbled upon this I have discovered It positively useful and it has aided me out loads. I hope to contribute & aid other customers like its aided me. Good job.

Thanks for the sensible critique. Me & my neighbor were just preparing to do a little research on this. We got a grab a book from our area library but I think I learned more from this post. I’m very glad to see such magnificent information being shared freely out there.

Hi my loved one! I want to say that this post is awesome, nice written and come with almost all vital infos. I’d like to look extra posts like this.

Dead pent subject matter, Really enjoyed examining.

An interesting discussion is worth comment. I think that you should write more on this topic, it might not be a taboo subject but generally people are not enough to speak on such topics. To the next. Cheers

I’ve read a few excellent stuff here. Certainly value bookmarking for revisiting. I surprise how so much effort you place to create this sort of wonderful informative site.

O Pix My Dollar é um aplicativo de microtarefas: você realiza atividades simples no celular e acumula recompensas, que podem ser convertidas em dinheiro.

F*ckin’ tremendous things here. I’m very glad to see your article. Thanks a lot and i’m looking forward to contact you. Will you kindly drop me a e-mail?

Se você gosta de fazer compras online e quer pagar menos sem abrir mão da qualidade, o Cupom da Vez é a solução ideal!

Whats Taking place i am new to this, I stumbled upon this I have discovered It positively useful and it has aided me out loads. I am hoping to give a contribution & assist other users like its helped me. Great job.

Thank you for the auspicious writeup. It in fact was a amusement account it. Look advanced to more added agreeable from you! However, how can we communicate?

Excellent website. Lots of useful info here. I¦m sending it to several pals ans also sharing in delicious. And obviously, thanks on your sweat!

Some truly great information, Glad I noticed this. “Be true to your work, your word, and your friend.” by Henry David Thoreau.

O Pix My Dollar é um aplicativo de microtarefas: você realiza atividades simples no celular e acumula recompensas, que podem ser convertidas em dinheiro.

I simply desired to say thanks yet again. I do not know what I might have handled without the actual opinions contributed by you on such field. This was a real horrifying problem for me, but taking a look at the very professional style you solved that forced me to weep with delight. Now i’m thankful for this advice and as well , wish you comprehend what an amazing job you are undertaking teaching men and women all through your web blog. More than likely you have never come across any of us.

O Pix My Dollar é um aplicativo de microtarefas: você realiza atividades simples no celular e acumula recompensas, que podem ser convertidas em dinheiro.

Today, I went to the beach with my kids. I found a sea shell and gave it to my 4 year old daughter and said “You can hear the ocean if you put this to your ear.” She put the shell to her ear and screamed. There was a hermit crab inside and it pinched her ear. She never wants to go back! LoL I know this is completely off topic but I had to tell someone!

You can certainly see your skills in the work you write. The arena hopes for even more passionate writers like you who aren’t afraid to mention how they believe. At all times go after your heart.

Simply a smiling visitor here to share the love (:, btw outstanding style and design.

Thanks for all your valuable labor on this website. Debby delights in going through investigation and it is obvious why. Many of us learn all relating to the lively manner you make important tricks on this blog and therefore increase response from visitors on that matter while our favorite princess has been being taught a whole lot. Take pleasure in the rest of the year. Your doing a fantastic job.

O Pix My Dollar é um aplicativo de microtarefas: você realiza atividades simples no celular e acumula recompensas, que podem ser convertidas em dinheiro.

After study a few of the blog posts on your website now, and I truly like your way of blogging. I bookmarked it to my bookmark website list and will be checking back soon. Pls check out my web site as well and let me know what you think.

This is a very good tips especially to those new to blogosphere, brief and accurate information… Thanks for sharing this one. A must read article.

That is very fascinating, You’re an excessively skilled blogger. I have joined your feed and sit up for looking for more of your wonderful post. Additionally, I have shared your site in my social networks!

I love the efforts you have put in this, thanks for all the great blog posts.

Virtue, they say, lies in the middle, but who among us can truly say where the middle is? Is it a fixed point, or does it shift with time, perception, and context? Perhaps the middle is not a place but a way of moving, a constant balancing act between excess and deficiency. Maybe to be virtuous is not to reach the middle but to dance around it with grace.

Man is said to seek happiness above all else, but what if true happiness comes only when we stop searching for it? It is like trying to catch the wind with our hands—the harder we try, the more it slips through our fingers. Perhaps happiness is not a destination but a state of allowing, of surrendering to the present and realizing that we already have everything we need.

Very good blog you have here but I was curious if you knew of any community forums that cover the same topics discussed here? I’d really love to be a part of online community where I can get advice from other experienced individuals that share the same interest. If you have any recommendations, please let me know. Thanks a lot!

I am always thought about this, appreciate it for posting.

Having read this I thought it was very informative. I appreciate you taking the time and effort to put this article together. I once again find myself spending way to much time both reading and commenting. But so what, it was still worth it!

I’ve been surfing on-line greater than three hours today, but I by no means found any attention-grabbing article like yours. It is lovely value enough for me. Personally, if all webmasters and bloggers made excellent content as you did, the web will be a lot more useful than ever before.

Does your site have a contact page? I’m having problems locating it but, I’d like to send you an e-mail. I’ve got some recommendations for your blog you might be interested in hearing. Either way, great site and I look forward to seeing it expand over time.

I’m extremely impressed together with your writing abilities and also with the layout for your weblog. Is that this a paid subject matter or did you customize it your self? Anyway stay up the excellent high quality writing, it’s uncommon to see a great blog like this one nowadays..

I think this is one of the most important information for me. And i’m glad reading your article. But should remark on some general things, The website style is perfect, the articles is really excellent : D. Good job, cheers

Somebody essentially assist to make seriously articles I might state. This is the first time I frequented your web page and thus far? I surprised with the research you made to make this particular submit extraordinary. Excellent process!

Wohh just what I was looking for, thanks for posting.

Nice post. I learn something more challenging on different blogs everyday. It will always be stimulating to read content from other writers and practice a little something from their store. I’d prefer to use some with the content on my blog whether you don’t mind. Natually I’ll give you a link on your web blog. Thanks for sharing.

Terrific post however I was wondering if you could write a litte more on this subject? I’d be very grateful if you could elaborate a little bit further. Thank you!

Good – I should definitely pronounce, impressed with your website. I had no trouble navigating through all tabs as well as related information ended up being truly easy to do to access. I recently found what I hoped for before you know it at all. Quite unusual. Is likely to appreciate it for those who add forums or something, web site theme . a tones way for your customer to communicate. Excellent task.

Some truly wonderful work on behalf of the owner of this internet site, absolutely outstanding content.

I am extremely impressed with your writing skills as well as with the layout on your blog. Is this a paid theme or did you customize it yourself? Either way keep up the excellent quality writing, it’s rare to see a nice blog like this one today..

Can I just say what a relief to find someone who actually knows what theyre talking about on the internet. You definitely know how to bring an issue to light and make it important. More people need to read this and understand this side of the story. I cant believe youre not more popular because you definitely have the gift.

Would you be fascinated by exchanging hyperlinks?

Some genuinely interesting details you have written.Helped me a lot, just what I was searching for : D.

I’ve been surfing on-line greater than three hours today, yet I by no means discovered any attention-grabbing article like yours. It is lovely value enough for me. In my view, if all website owners and bloggers made good content as you did, the internet will probably be a lot more useful than ever before. “When there is a lack of honor in government, the morals of the whole people are poisoned.” by Herbert Clark Hoover.

Lovely just what I was looking for.Thanks to the author for taking his clock time on this one.

Would love to perpetually get updated outstanding weblog! .

You really make it seem so easy with your presentation but I find this matter to be really something that I think I would never understand. It seems too complicated and very broad for me. I’m looking forward for your next post, I will try to get the hang of it!

When I originally commented I clicked the “Notify me when new comments are added” checkbox and now each time a comment is added I get several emails with the same comment. Is there any way you can remove me from that service? Thanks!

Hello my family member! I want to say that this article is amazing, nice written and include almost all significant infos. I?¦d like to look more posts like this .

That is the best weblog for anyone who desires to find out about this topic. You understand so much its nearly laborious to argue with you (not that I truly would need…HaHa). You definitely put a brand new spin on a subject thats been written about for years. Nice stuff, just great!

Have you ever considered about adding a little bit more than just your articles? I mean, what you say is valuable and everything. But think of if you added some great photos or videos to give your posts more, “pop”! Your content is excellent but with images and videos, this site could undeniably be one of the best in its field. Superb blog!

Perfectly written subject material, thankyou for information .

Youre so cool! I dont suppose Ive learn something like this before. So nice to seek out someone with some original thoughts on this subject. realy thank you for starting this up. this website is something that is needed on the net, somebody with somewhat originality. useful job for bringing one thing new to the internet!

I have learn a few good stuff here. Definitely value bookmarking for revisiting. I wonder how a lot effort you set to create such a magnificent informative website.

I have recently started a site, the info you provide on this web site has helped me greatly. Thanks for all of your time & work. “The man who fights for his fellow-man is a better man than the one who fights for himself.” by Clarence Darrow.

An interesting discussion is worth comment. I think that you should write more on this topic, it might not be a taboo subject but generally people are not enough to speak on such topics. To the next. Cheers

Hey there! Someone in my Facebook group shared this website with us so I came to give it a look. I’m definitely loving the information. I’m book-marking and will be tweeting this to my followers! Outstanding blog and terrific style and design.

Good info. Lucky me I reach on your website by accident, I bookmarked it.

hello!,I like your writing very much! share we communicate more about your post on AOL? I require a specialist on this area to solve my problem. Maybe that’s you! Looking forward to see you.

As a Newbie, I am permanently exploring online for articles that can help me. Thank you

I will right away take hold of your rss as I can not in finding your email subscription link or newsletter service. Do you’ve any? Please permit me recognize in order that I may subscribe. Thanks.

I carry on listening to the news lecture about getting boundless online grant applications so I have been looking around for the finest site to get one. Could you tell me please, where could i get some?

Please let me know if you’re looking for a article writer for your blog. You have some really good posts and I believe I would be a good asset. If you ever want to take some of the load off, I’d really like to write some content for your blog in exchange for a link back to mine. Please send me an e-mail if interested. Thank you!

Hey! Do you know if they make any plugins to assist with SEO? I’m trying to get my blog to rank for some targeted keywords but I’m not seeing very good gains. If you know of any please share. Appreciate it!

I’ve read some just right stuff here. Definitely value bookmarking for revisiting. I wonder how much effort you put to make this sort of magnificent informative site.

Terrific work! This is the kind of information that should be shared across the internet. Shame on the search engines for no longer positioning this publish upper! Come on over and visit my site . Thanks =)

I truly enjoy reading through on this website, it contains wonderful content. “The living is a species of the dead and not a very attractive one.” by Friedrich Wilhelm Nietzsche.

Hi my friend! I want to say that this post is awesome, great written and come with approximately all vital infos. I?¦d like to peer more posts like this .

Thank you for your own work on this web site. Gloria really likes going through investigation and it’s really easy to see why. Many of us learn all regarding the powerful method you give helpful strategies on the blog and even cause participation from others on the area of interest while our favorite simple princess is undoubtedly being taught a lot. Have fun with the rest of the new year. You’re carrying out a good job.

If everything in this universe has a cause, then surely the cause of my hunger must be the divine order of things aligning to guide me toward the ultimate pleasure of a well-timed meal. Could it be that desire itself is a cosmic signal, a way for nature to communicate with us, pushing us toward the fulfillment of our potential? Perhaps the true philosopher is not the one who ignores his desires, but the one who understands their deeper meaning.

Thanks – Enjoyed this blog post, can I set it up so I get an email sent to me whenever you write a new update?

I really like your writing style, excellent information, regards for posting : D.

Well I really enjoyed reading it. This article procured by you is very useful for correct planning.

Excellent blog! Do you have any helpful hints for aspiring writers? I’m planning to start my own blog soon but I’m a little lost on everything. Would you recommend starting with a free platform like WordPress or go for a paid option? There are so many options out there that I’m completely confused .. Any ideas? Thanks!

This web site is really a walk-through for all of the info you wanted about this and didn’t know who to ask. Glimpse here, and you’ll definitely discover it.

I like what you guys are up also. Such smart work and reporting! Keep up the superb works guys I’ve incorporated you guys to my blogroll. I think it will improve the value of my website :).

I would like to get across my love for your generosity in support of individuals that must have guidance on that situation. Your very own dedication to getting the message throughout came to be particularly interesting and has continually permitted those just like me to get to their ambitions. The interesting guideline implies this much to me and especially to my office workers. With thanks; from all of us.

I was very pleased to find this web-site.I wanted to thanks for your time for this wonderful read!! I definitely enjoying every little bit of it and I have you bookmarked to check out new stuff you blog post.

I’ve been absent for some time, but now I remember why I used to love this web site. Thanks, I will try and check back more often. How frequently you update your website?

Hello my friend! I want to say that this post is amazing, nice written and include approximately all important infos. I’d like to see more posts like this.

Fantastic site you have here but I was curious if you knew of any discussion boards that cover the same topics talked about here? I’d really love to be a part of online community where I can get comments from other knowledgeable individuals that share the same interest. If you have any recommendations, please let me know. Many thanks!

Enjoyed looking at this, very good stuff, thankyou.

It is actually a great and helpful piece of information. I?¦m satisfied that you just shared this helpful information with us. Please stay us up to date like this. Thank you for sharing.

You are my inspiration , I have few blogs and very sporadically run out from to post .

As I site possessor I believe the content matter here is rattling excellent , appreciate it for your efforts. You should keep it up forever! Best of luck.

Hi, I think your site might be having browser compatibility issues. When I look at your website in Safari, it looks fine but when opening in Internet Explorer, it has some overlapping. I just wanted to give you a quick heads up! Other then that, fantastic blog!

I am not positive the place you’re getting your info, however great topic. I needs to spend a while finding out more or working out more. Thanks for fantastic information I was in search of this info for my mission.

There is obviously a bundle to realize about this. I consider you made various nice points in features also.

I like this post, enjoyed this one thank you for posting. “No trumpets sound when the important decisions of our life are made. Destiny is made known silently.” by Agnes de Mille.

Thank you for sharing superb informations. Your site is very cool. I’m impressed by the details that you¦ve on this web site. It reveals how nicely you understand this subject. Bookmarked this website page, will come back for more articles. You, my friend, ROCK! I found just the information I already searched everywhere and simply couldn’t come across. What a great web-site.

I was suggested this blog by my cousin. I am not sure whether this post is written by him as nobody else know such detailed about my problem. You’re amazing! Thanks!

Thankyou for this post, I am a big big fan of this site would like to continue updated.

This is the right blog for anyone who wants to find out about this topic. You realize so much its almost hard to argue with you (not that I actually would want…HaHa). You definitely put a new spin on a topic thats been written about for years. Great stuff, just great!

Some truly good info , Glad I observed this. “The past is a guide post, not a hitching post.” by L. Thomas Holdcroft.

Hi my friend! I want to say that this article is amazing, nice written and include approximately all vital infos. I would like to see more posts like this.

Hello my family member! I want to say that this article is amazing, nice written and come with almost all significant infos. I would like to peer more posts like this.

The Salt Trick is a natural technique that involves using specific salts, such as Blue Salt, to enhance male performance

Great write-up, I¦m regular visitor of one¦s web site, maintain up the excellent operate, and It is going to be a regular visitor for a lengthy time.

The Natural Mounjaro Recipe is more than just a diet—it’s a sustainable and natural approach to weight management and overall health.

The Natural Mounjaro Recipe is more than just a diet—it’s a sustainable and natural approach to weight management and overall health.

I’ve been absent for a while, but now I remember why I used to love this web site. Thanks , I will try and check back more frequently. How frequently you update your site?

Mitolyn is a cutting-edge natural dietary supplement designed to support effective weight loss and improve overall wellness.

Does your site have a contact page? I’m having problems locating it but, I’d like to send you an email. I’ve got some suggestions for your blog you might be interested in hearing. Either way, great website and I look forward to seeing it grow over time.

This blog is definitely rather handy since I’m at the moment creating an internet floral website – although I am only starting out therefore it’s really fairly small, nothing like this site. Can link to a few of the posts here as they are quite. Thanks much. Zoey Olsen

ProDentim is a chewable oral probiotic supplement formulated with a unique mix of probiotics, prebiotics, herbs, and nutrients.

I went over this site and I believe you have a lot of excellent information, saved to favorites (:.

Perfect work you have done, this site is really cool with superb info .

Hey very cool website!! Man .. Beautiful .. Wonderful .. I will bookmark your web site and take the feeds also…I’m glad to seek out numerous helpful info right here within the post, we’d like develop more strategies in this regard, thanks for sharing. . . . . .

Hey very cool web site!! Man .. Excellent .. Amazing .. I will bookmark your site and take the feeds also…I’m happy to find numerous useful info here in the post, we need develop more strategies in this regard, thanks for sharing. . . . . .

Hi there, just changed into alert to your weblog thru Google, and located that it is really informative. I’m going to watch out for brussels. I’ll appreciate for those who continue this in future. Many other people will be benefited out of your writing. Cheers!

Good post and straight to the point. I am not sure if this is actually the best place to ask but do you folks have any ideea where to get some professional writers? Thanks 🙂

F*ckin¦ tremendous things here. I¦m very glad to look your article. Thank you a lot and i’m looking forward to touch you. Will you kindly drop me a e-mail?

Real informative and wonderful anatomical structure of articles, now that’s user pleasant (:.

I am forever thought about this, regards for putting up.

My spouse and I absolutely love your blog and find a lot of your post’s to be exactly I’m looking for. Does one offer guest writers to write content for you? I wouldn’t mind writing a post or elaborating on most of the subjects you write in relation to here. Again, awesome blog!

Hello! I just would like to give a huge thumbs up for the great info you have here on this post. I will be coming back to your blog for more soon.

I am extremely impressed with your writing skills and also with the layout on your weblog. Is this a paid theme or did you modify it yourself? Anyway keep up the excellent quality writing, it is rare to see a great blog like this one nowadays..

Hello There. I found your blog using msn. This is an extremely well written article. I will be sure to bookmark it and return to read more of your useful information. Thanks for the post. I will definitely comeback.

I don’t even understand how I stopped up right here, but I believed this post was good. I do not recognise who you are however certainly you are going to a well-known blogger in the event you are not already 😉 Cheers!

Woh I enjoy your posts, saved to bookmarks! .

What i don’t understood is if truth be told how you’re now not really a lot more well-liked than you may be now. You’re very intelligent. You already know therefore significantly relating to this matter, made me personally believe it from so many various angles. Its like women and men don’t seem to be involved except it is something to do with Lady gaga! Your own stuffs nice. At all times care for it up!

The next time I read a blog, I hope that it doesnt disappoint me as much as this one. I mean, I know it was my choice to read, but I actually thought youd have something interesting to say. All I hear is a bunch of whining about something that you could fix if you werent too busy looking for attention.

Compre visualizações e espectadores reais para suas lives no YouTube, Instagram, Twitch, TikTok e Facebook. Aumente seu engajamento e credibilidade online com serviços seguros e confiáveis. Impulsione suas transmissões ao vivo hoje!

Thanks for helping out, excellent info .