This site contains affiliate links to products. I may receive a commission for purchases made through these links, at no additional cost to you. As an Amazon Associate I earn from qualifying purchases. Read my disclaimers page for more information.

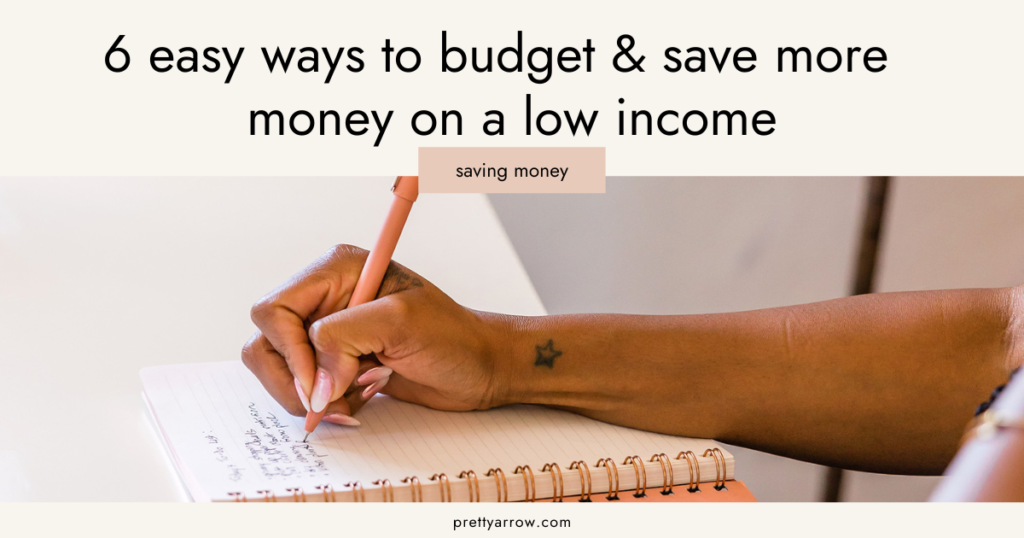

Trying to budget on a low income can feel like a challenge.

You might be living paycheck to paycheck, you could be behind on your bills, and you might end up maxed out on your credit cards.

I can tell you this used to describe my life, especially when I had just graduated college and was working entry-level jobs (most of the time, earning minimum wage or close to it).

The good news is that a budget can help you reach your goals, even with a low income.

Having a plan for your money is a great way to stress less (and start focusing on other things in life!).

Here are six steps you can take to stop living paycheck to paycheck (and save more money) on a low income:

1. Make a zero-based budget

When you make a plan for each dollar you make, you are following a zero-based budget. With zero-based budgeting, your income minus your expenses equals zero.

This means you are including every expense you have in your budget, including room for miscellaneous spending (or spending you haven’t necessarily planned for).

Having a zero-based budget is important when you have a low income for a few reasons:

-You can make sure you’re covering everything you need to, like bills, groceries, debt repayments and savings goals

-You’ll have a clear picture of where all of your money is going. This makes it easy to see where you could cut back on spending or if you should eliminate an expense entirely

For example, if you see that you’re spending over half of your income on rent- this might not be the best way to use 50% of your income. That’s a big chunk of your money going to one expense- which doesn’t leave a lot to cover everything else in your life.

You might decide to downsize your apartment or get a roommate to make sure you have enough room in your budget for everything.

How to take action:

Making a zero-based budget is easy! Like I mentioned before, you only need to make sure your income minus your expenses is zero.

1.Pick a budgeting method that works for you, whether that is writing it down on paper or making a digital budget with a spreadsheet.

If you’re new to budgeting, you can use a budget spreadsheet to automatically calculate what you’re spending in each area of your budget.

Our budget spreadsheets all include expense trackers that do this for you. Simply enter what you spent at the end of each day (it only takes 5 minutes!), and you can easily see how much you have left to spend in each category (like groceries, dining out, utilities, shopping, etc.)

It’s a much easier way to track your spending (compared to adding it up with a calculator for each category), so it’s also an easier habit to stick to.

You’ll find our ready-to-go budget printables and spreadsheets here.

2. Decide how often you want to budget, either by month or by paycheck.

You can make a budget for the entire month in advance, or you can budget for each paycheck when you get paid.

If you go with a monthly budget, you only need to put a budget together once a month. However, it can be harder to predict your spending for an entire month in advance.

If you decide to budget by paycheck, you will be making a budget more often- but it’s a little easier to predict what you need to buy for the next week or two (depending on how often you get paid).

3. Include 5 basic budgeting categories each time

There are 5 budget categories that you should include in your budget:

- Your income, ie. your paycheck, a tax return, a bonus at work

- Your monthly bills, ie. rent/mortgage payment, phone bill, internet bill, insurance payments, minimum required payments on credit cards or student loans.

Tips to never be late on a bill again:

–List your bill due dates in your budget

–Automate your bill payments, so they are withdrawn from your bank account automatically when they are due

–Use a monthly calendar to record your bill due dates and paydays (this makes it easy to see what bills you need to cover with each paycheck)

- Your variable expenses/spending, ie. groceries, dining out, fuel, utilities, shopping, gifts, home expenses, personal care, etc.

- Contributions to your savings, ie. saving money for a rainy day (your emergency fund), saving up for a big purchase (your sinking funds), etc.

- Extra debt repayments, ie. making extra payments on your debt, above and beyond the minimum payments, so you can pay them off faster

Our Zero-Based Budgeting Templates:

Ultimate Budget by Paycheck template (includes a budget template, expense tracker, monthly calendar for your bills, sinking funds tracker, and a debt snowball calculator to find out when you’ll be debt-free)

Ultimate Monthly Budget template (includes a budget template, expense tracker, monthly calendar for your bills, sinking funds tracker, and a debt snowball calculator to find out when you’ll be debt-free)

Budget by Paycheck printable template

Monthly Budget printable template

4. Know your budget percentages

When you’re working with a limited income, it’s extra important to know what percentage of your money is going where.

Although it’s impossible to say how exactly much you should spend in each budget category (everyone’s situation is unique), there are some rough guidelines you can keep in mind:

Housing 25%

Utilities 5-10%

Transportation 10%

Food 10-15%

Insurance 10%

Entertainment 5-10%

Personal Care 5-10%

Health/Medical 5-10%

Shopping 5-10%

Miscellaneous 5-10%

Savings 10-15%

Other categories, like debt, child care, or tuition, can be added in depending on if these expenses apply to you.

Check out our free guide to budget categories and budget percentages here.

2. Prioritize your essential monthly bills

Monthly bills are your fixed, recurring expenses that you know you need to pay each month.

Some of your monthly bills are absolutely essential, like housing and utility bills- these are the ones that you need to live.

If you don’t pay these bills, there could be serious consequences.

It’s important to ensure these bills are covered (and are paid on time) before worrying about your other bills.

Examples of your non-essential monthly bills are things like gym memberships, music or movie subscriptions, or online membership fees.

These are bills that you can cancel if you need to cover the bigger priorities in your budget.

How to take action:

Pay your essential monthly bills first, before any non-essential ones.

Once you make your budget, go through your list of recurring bills and see if there are any you can cancel. This could be because it’s a subscription you’re not using, or one that you don’t use enough to justify the price.

There are other bills that you can’t cancel, but that can be reduced by negotiating a lower price or switching to a cheaper plan.

Examples of this are your phone and internet bills.

The reason it’s important to review your monthly bill costs is because these are predictable expenses that are coming out every time you get paid. If you can reduce them, you can save money continually each month!

Tools + resources to help you save money on your monthly bills:

Trim is a powerful tool that helps you to cancel old subscriptions, negotiate lower prices on your bills, and save money on your monthly spending. It even analyzes your spending patterns for you so you can see where you can save money every month!

3. Start to track your spending

Your variable expenses are the costs you have that tend to change each month- think of them as your spending costs. Examples of things you spend money on are groceries, shopping, and transportation.

The two biggest variable expenses for most people are groceries and transportation (housing is usually the biggest expense of all, but that is a monthly bill).

If you’re not sure how to track your spending or if you feel overwhelmed by tracking it all, focus on your grocery and transportation spending. This is likely where most of your money is being spent.

How to take action: Use your last 30 days of bank account and credit card statements to see how much you are spending.

Take a closer look and see what your top 3-5 spending categories are.

By focusing on spending less in these areas, you can save money quickly!

That being said, don’t ignore the smaller expenses that might just be mindless spending or spending that is completely unnecessary- cutting out this kind of spending will also have an impact.

Tools + resources to help you save money on your variable expenses:

5 Dollar Meal Plan – a meal planning service that sends you a month’s worth of cheap recipes and grocery lists for $5 a month. Since each recipe is designed to be frugal and inexpensive, you can easily stick to your food budget without resorting to bland, boring meals!

Meal Planning Printables – a bundle of six meal prep printables you can print off at home

Drop – a rewards program that links to your debit or credit card- you’ll earn points every time you shop at your favourite retailers, which can be turned into gift cards. You can earn extra points by taking surveys and playing games, too.

Swagbucks – Swagbucks is one of my favourite ways to earn free gift cards online! (it takes less than a minute to sign up) and start to earn rewards for things you’re already doing, like surfing the web and shopping online. You’ll even be rewarded for answering surveys & watching videos! Your rewards can be redeemed for gift cards at popular retailers you’re probably already shopping at, like Amazon, Walmart, and Starbucks.

4. Save an emergency fund

An emergency fund is essentially your rainy day fund- it’s savings for unexpected expenses, like losing your job or your car needing major repairs.

It is recommended to have 3-6 months’ worth of necessary living expenses (think rent and food, not entertainment and shopping) saved here.

When you feel like money is tight, saving for an emergency fund might be the last thing on your mind. But having one in place, even if it’s small- can alleviate a lot of money stress.

Many of us are using our credit cards as emergency funds without realizing it. When something unexpected happens, we pay for it with our cards.

This habit puts you further into debt, which also increases your minimum payments on your credit cards. Remember that we’re trying to reduce your monthly costs- not increase them!

Even if you can only cover part of an expense with your savings, you’re still racking up less debt than you might have otherwise.

P.S. if you do have debt you are working on paying off, you can save up a smaller amount for emergencies (ie. $1,000), just until you are debt-free. Once the debt is gone, you can save up more.

How to take action: Open a free, no-fee savings account with your bank (a basic savings account will work just fine- you’ll want to be able to access this money quickly if an emergency comes up).

Add up your necessary monthly living expenses, and multiply this number by 3-6 to find out how much you need to save in your emergency fund.

Pssst- we have an emergency fund calculator in our Free Budget Resource Library that you can use to figure this out!

Include regular contributions to your emergency fund in your budget. Even if it’s only a small amount, this is still a really important goal to start working towards.

5. Make a plan to pay off your debt

Having an emergency fund helps to keep you out of debt.

Going into debt means more monthly payments on things like credit cards, lines of credit, student loans, etc.

Imagine if you didn’t have these monthly debt repayments– that could give you a lot more wiggle room in your budget.

Plus, you’re being charged interest on this debt, which is more money down the drain.

It’s important to try to avoid racking up large amounts of debt, and it’s even better to pay it off!

How to take action:

Change your spending mindset– instead of putting things you can’t afford on a credit card, start a spending wish list. This is a list of all the things you want to buy and their prices- save up the money for each item, and buy it in cash when you can afford it.

Make a plan to pay off your debt. Start by listing all of your debts, including the amounts owing and what the minimum monthly payments are.

Focus on paying off one debt at a time- when you’re done paying one off, roll its monthly payment into the next debt until it is paid off. Repeat until debt free!

There are two commonly used debt repayment methods:

The Debt Snowball Method (more on that here– this is the debt payoff method I used!): Pay your debts off in order from the smallest amount owing to the largest. This method is great for staying motivated because you can pay off the smallest debt the fastest- you’ll feel great once you’ve paid it all off, and you’ll want to keep going!

The Debt Avalanche Method: Pay off your debts in order from the highest interest rate to the lowest. This method could work for you if you are motivated to stop paying a ton of money in interest on your debt. It could also work if all of your debts have the same (or very similar) amounts owing.

While you’re paying off debt, it’s also a good practice to reduce mindless spending (so you’ll have as much money as possible to pay off your debt with).

Here a few ways you can save money during this time:

–Try not to buy brand-new items– instead, try to only buy used or second-hand items when you need to buy something. If you can’t find a second-hand version, shop around for the cheapest option online.

–Only buy the necessities or things that you need. You can try a no-spend challenge for 7, 14, or 30 days to boost your savings- during this time period, you only buy the things that you need.

–Start to buy groceries at bulk stores or discount stores like Walmart or dollar stores

–Plan the days in a week you can afford to eat out. For the other days, plan out your meals in advance and spend 1-2 days a week meal prepping for the days ahead.

6. Do an expense audit every 3-6 months

An expense audit is where you go through each of your bills and expenses one-by-one and see where you can save money.

This could be by cancelling a subscription, trying to spend less on eating out, or by calling your cell phone provider and negotiating a cheaper phone bill.

By planning to have regular expense audits during the year, you can make sure you’re always spending as little as possible.

How to take action: Do an expense audit with your first budget, and then every 3-6 months after that.

Your expenses and bills will change, and it’s important to make sure you’re not paying for something you don’t use, or overpaying for something you do need.

Expense Audit Tools:

Printable Expense Audit tracker (included in our printable Budget Planner)

Digital Expense Audit tracker (included in our Bill Tracker spreadsheet)

Free Budgeting Resources:

Free Budget Resource Library – our library of budgeting printables & spreadsheets is completely free to sign up for! We’re always adding new tools to the library to help you budget better (without spending a dime).

Credit Karma – is a completely free way to check your credit score online. I’ve been using Credit Karma for years and I love how they also give you detailed feedback on how you can improve your score.

Mint – a free budgeting app that lets you plan your budget and track all of your spending on your phone.

I am enjoying reading your posts after having just discovered your blog tonight. BUT the print is a very light gray, and except where you have highlighted, the words are really hard to read. I see you have put a lot of thought and hard work into your blog so I just wanted to make you aware of this. Keep up the good work!

Thank you for sharing this insightful article! I found the information really useful and thought-provoking. Your writing style is engaging, and it made the topic much easier to understand. Looking forward to reading more of your posts!

x42lx9

8o8kjp

I got what you mean , appreciate it for putting up.Woh I am pleased to find this website through google.

Really fantastic visual appeal on this site, I’d rate it 10 10.

qkftdh

Somebody essentially lend a hand to make seriously articles I’d state. This is the first time I frequented your web page and thus far? I amazed with the analysis you made to make this actual submit extraordinary. Magnificent job!

is6oxf

I’m no longer certain the place you are getting your information, but good topic. I must spend a while finding out more or working out more. Thanks for great information I was searching for this info for my mission.

Howdy! Do you know if they make any plugins to help with SEO? I’m trying to get my blog to rank for some targeted keywords but I’m not seeing very good results. If you know of any please share. Thanks!

wmu7sb

Simply a smiling visitor here to share the love (:, btw outstanding style and design. “Individuals may form communities, but it is institutions alone that can create a nation.” by Benjamin Disraeli.

I have recently started a web site, the information you provide on this website has helped me greatly. Thanks for all of your time & work. “Character is much easier kept than recovered.” by Thomas Paine.

waeu3l

Really superb information can be found on website.

Excellent read, I just passed this onto a colleague who was doing some research on that. And he actually bought me lunch as I found it for him smile So let me rephrase that: Thanks for lunch!

I was more than happy to seek out this net-site.I wished to thanks for your time for this glorious learn!! I undoubtedly enjoying every little bit of it and I have you bookmarked to check out new stuff you weblog post.

Real good visual appeal on this internet site, I’d value it 10 10.

With havin so much written content do you ever run into any problems of plagorism or copyright infringement? My blog has a lot of exclusive content I’ve either created myself or outsourced but it looks like a lot of it is popping it up all over the web without my agreement. Do you know any ways to help prevent content from being stolen? I’d really appreciate it.

I have recently started a site, the info you provide on this website has helped me tremendously. Thank you for all of your time & work.

I’ve been absent for some time, but now I remember why I used to love this blog. Thank you, I will try and check back more frequently. How frequently you update your web site?

Do you have a spam problem on this website; I also am a blogger, and I was wondering your situation; many of us have developed some nice practices and we are looking to exchange methods with other folks, be sure to shoot me an e-mail if interested.

1k44ze

I am now not certain where you are getting your information, however good topic. I needs to spend some time finding out more or working out more. Thank you for wonderful info I used to be looking for this information for my mission.

I’ve recently started a website, the info you provide on this website has helped me tremendously. Thanks for all of your time & work.

Some genuinely fantastic articles on this website, regards for contribution. “It is not often that someone comes along who is a true friend and a good writer.” by E. B. White.

Sweet website , super design, really clean and use pleasant.

We stumbled over here coming from a different web page and thought I might as well check things out. I like what I see so now i am following you. Look forward to going over your web page again.

It is really a nice and helpful piece of info. I?¦m satisfied that you just shared this useful info with us. Please stay us informed like this. Thank you for sharing.

I really like your writing style, excellent information, thanks for putting up :D. “Faith is a continuation of reason.” by William Adams.

I haven?¦t checked in here for a while because I thought it was getting boring, but the last several posts are good quality so I guess I?¦ll add you back to my daily bloglist. You deserve it my friend 🙂

I truly appreciate this post. I have been looking everywhere for this! Thank goodness I found it on Bing. You have made my day! Thx again

I believe this web site holds some very excellent information for everyone :D. “Anybody who watches three games of football in a row should be declared brain dead.” by Erma Bombeck.

My brother suggested I might like this web site. He was totally right. This post actually made my day. You cann’t imagine simply how much time I had spent for this info! Thanks!

Utterly indited subject material, regards for selective information. “In the fight between you and the world, back the world.” by Frank Zappa.

F*ckin’ amazing things here. I’m very glad to see your article. Thanks a lot and i’m looking forward to contact you. Will you kindly drop me a e-mail?

I was examining some of your articles on this website and I believe this internet site is rattling informative! Continue posting.

Wohh just what I was looking for, regards for putting up.

Would you be fascinated with exchanging links?

What i don’t realize is in reality how you are now not really a lot more smartly-liked than you might be now. You are so intelligent. You already know thus considerably in relation to this matter, produced me in my view consider it from so many numerous angles. Its like women and men aren’t involved except it’s one thing to do with Lady gaga! Your individual stuffs outstanding. At all times deal with it up!

s6pank

You are my inspiration , I have few blogs and very sporadically run out from to brand : (.

Enjoyed examining this, very good stuff, thankyou. “All things are difficult before they are easy.” by John Norley.

Its like you read my mind! You seem to know so much about this, like you wrote the book in it or something. I think that you could do with a few pics to drive the message home a bit, but instead of that, this is wonderful blog. An excellent read. I’ll certainly be back.

Hi there very nice blog!! Man .. Beautiful .. Superb .. I’ll bookmark your web site and take the feeds also?KI’m glad to search out a lot of useful info here in the post, we want develop more techniques on this regard, thanks for sharing. . . . . .

Hey! Someone in my Facebook group shared this site with us so I came to give it a look. I’m definitely enjoying the information. I’m bookmarking and will be tweeting this to my followers! Terrific blog and excellent design and style.

I got what you mean , appreciate it for putting up.Woh I am glad to find this website through google.

I’ve been absent for some time, but now I remember why I used to love this site. Thanks, I will try and check back more frequently. How frequently you update your web site?

Good blog! I really love how it is easy on my eyes and the data are well written. I’m wondering how I could be notified when a new post has been made. I’ve subscribed to your RSS which must do the trick! Have a great day!

You really make it seem so easy with your presentation but I find this matter to be actually something that I think I would never understand. It seems too complex and extremely broad for me. I’m looking forward for your next post, I will try to get the hang of it!

You completed several good points there. I did a search on the subject and found nearly all persons will have the same opinion with your blog.

I have recently started a blog, the information you offer on this site has helped me tremendously. Thanks for all of your time & work.

My coder is trying to persuade me to move to .net from PHP. I have always disliked the idea because of the expenses. But he’s tryiong none the less. I’ve been using Movable-type on various websites for about a year and am concerned about switching to another platform. I have heard great things about blogengine.net. Is there a way I can transfer all my wordpress content into it? Any kind of help would be really appreciated!

Thanks for another informative blog. Where else could I get that type of information written in such a perfect way? I have a project that I’m just now working on, and I’ve been on the look out for such information.

obviously like your website however you need to test the spelling on quite a few of your posts. Several of them are rife with spelling problems and I in finding it very troublesome to inform the reality on the other hand I will surely come back again.

I like what you guys are up also. Such intelligent work and reporting! Carry on the superb works guys I’ve incorporated you guys to my blogroll. I think it will improve the value of my site :).

I like this web blog its a master peace ! Glad I discovered this on google .

Very interesting details you have observed, regards for posting. “History is a cyclic poem written by Time upon the memories of man.” by Percy Bysshe Shelley.

I precisely had to thank you very much again. I’m not certain the things that I could possibly have worked on without the entire techniques shared by you directly on my area. Completely was a depressing concern in my opinion, however , being able to view a new well-written manner you processed it took me to leap over contentment. Now i am happy for your assistance and in addition trust you comprehend what a great job that you are doing teaching some other people via a web site. I am certain you haven’t met any of us.

You could certainly see your skills within the work you write. The sector hopes for more passionate writers like you who are not afraid to say how they believe. At all times go after your heart. “A second wife is hateful to the children of the first a viper is not more hateful.” by Euripides.

Good – I should certainly pronounce, impressed with your website. I had no trouble navigating through all the tabs and related info ended up being truly simple to do to access. I recently found what I hoped for before you know it at all. Reasonably unusual. Is likely to appreciate it for those who add forums or anything, website theme . a tones way for your client to communicate. Nice task.

After study a few of the weblog posts on your web site now, and I truly like your approach of blogging. I bookmarked it to my bookmark website record and can be checking back soon. Pls take a look at my web site as nicely and let me know what you think.

Do you mind if I quote a few of your posts as long as I provide credit and sources back to your webpage? My blog site is in the exact same area of interest as yours and my users would genuinely benefit from some of the information you present here. Please let me know if this alright with you. Regards!

I have been absent for some time, but now I remember why I used to love this web site. Thanks, I?¦ll try and check back more often. How frequently you update your site?

Greetings! Very helpful advice on this article! It is the little changes that make the biggest changes. Thanks a lot for sharing!

I conceive you have observed some very interesting points, regards for the post.

Thanks – Enjoyed this update, how can I make is so that I receive an email sent to me every time you write a fresh update?

Thank you, I’ve recently been looking for information approximately this subject for a while and yours is the best I’ve discovered so far. But, what concerning the bottom line? Are you positive about the source?

Hello my friend! I want to say that this post is awesome, nice written and include almost all important infos. I’d like to peer extra posts like this .

Some genuinely quality articles on this website , saved to fav.

This web page is really a walk-by for all the info you needed about this and didn’t know who to ask. Glimpse right here, and also you’ll positively uncover it.

Hi, just required you to know I he added your site to my Google bookmarks due to your layout. But seriously, I believe your internet site has 1 in the freshest theme I??ve came across. It extremely helps make reading your blog significantly easier.

Hello my family member! I wish to say that this post is amazing, great written and include approximately all vital infos. I¦d like to peer more posts like this .

Thanks for helping out, great info .

When I initially commented I clicked the “Notify me when new comments are added” checkbox and now each time a comment is added I get four emails with the same comment. Is there any way you can remove people from that service? Bless you!

Enjoyed looking through this, very good stuff, thanks.

I do not even know how I ended up here, but I thought this post was great. I don’t know who you are but certainly you’re going to a famous blogger if you are not already 😉 Cheers!

You made some good points there. I did a search on the subject and found mainly persons will have the same opinion with your blog.

This is a topic close to my heart cheers, where are your contact details though?

I like this web site so much, saved to fav.

Undeniably believe that which you stated. Your favourite reason seemed to be at the internet the simplest thing to bear in mind of. I say to you, I certainly get annoyed whilst people think about concerns that they just do not recognise about. You controlled to hit the nail upon the highest and defined out the whole thing with no need side-effects , other people could take a signal. Will likely be again to get more. Thank you

fantastic publish, very informative. I wonder why the other specialists of this sector don’t notice this. You should continue your writing. I am confident, you have a huge readers’ base already!

I’ve been absent for some time, but now I remember why I used to love this website. Thank you, I will try and check back more frequently. How frequently you update your site?

In the grand pattern of things you receive a B+ just for effort and hard work. Exactly where you actually confused everybody ended up being on your specifics. As they say, details make or break the argument.. And it could not be much more true at this point. Having said that, permit me tell you exactly what did work. The writing is certainly incredibly powerful and this is possibly why I am making an effort in order to opine. I do not really make it a regular habit of doing that. Second, whilst I can easily notice the leaps in reason you make, I am not convinced of exactly how you appear to connect the ideas that make the conclusion. For the moment I will, no doubt yield to your position but trust in the future you connect the dots much better.

What¦s Happening i am new to this, I stumbled upon this I’ve found It absolutely helpful and it has aided me out loads. I am hoping to give a contribution & aid other customers like its aided me. Great job.

Thanks for another informative web site. Where else could I get that type of info written in such a perfect way? I have a project that I’m just now working on, and I’ve been on the look out for such information.

Purdentix reviews

Purdentix review

Purdentix review

I have been exploring for a little for any high-quality articles or blog posts on this kind of space . Exploring in Yahoo I finally stumbled upon this site. Studying this information So i am glad to show that I have an incredibly good uncanny feeling I discovered just what I needed. I most undoubtedly will make sure to do not forget this website and give it a glance on a relentless basis.

Purdentix reviews

Purdentix review

Fascinating blog! Is your theme custom made or did you download it from somewhere? A theme like yours with a few simple adjustements would really make my blog stand out. Please let me know where you got your theme. With thanks

Purdentix review

Purdentix reviews

Purdentix review

Purdentix reviews

I love how user-friendly and intuitive everything feels.

A perfect blend of aesthetics and functionality makes browsing a pleasure.

A perfect blend of aesthetics and functionality makes browsing a pleasure.

Keep up the wonderful work, I read few blog posts on this internet site and I think that your site is rattling interesting and holds sets of fantastic info .

Would you be excited about exchanging links?

It provides an excellent user experience from start to finish.

I love how user-friendly and intuitive everything feels.

It provides an excellent user experience from start to finish.

This website is amazing, with a clean design and easy navigation.

This website is amazing, with a clean design and easy navigation.

Some truly interesting details you have written.Aided me a lot, just what I was searching for : D.

The content is well-organized and highly informative.

The layout is visually appealing and very functional.

The layout is visually appealing and very functional.

This site truly stands out as a great example of quality web design and performance.

The design and usability are top-notch, making everything flow smoothly.

This website is amazing, with a clean design and easy navigation.

The content is engaging and well-structured, keeping visitors interested.

It provides an excellent user experience from start to finish.

Rattling instructive and fantastic structure of subject material, now that’s user genial (:.

I’m really impressed by the speed and responsiveness.

The content is engaging and well-structured, keeping visitors interested.

I have been surfing on-line more than 3 hours nowadays, yet I by no means discovered any interesting article like yours. It’s beautiful value sufficient for me. In my opinion, if all webmasters and bloggers made just right content as you did, the net shall be a lot more useful than ever before.

You have brought up a very excellent details , thanks for the post.

I’d need to verify with you here. Which is not one thing I often do! I take pleasure in studying a post that may make people think. Also, thanks for allowing me to remark!

Hi, Neat post. There is a problem with your website in internet explorer, may test this… IE still is the marketplace leader and a large component of other folks will omit your wonderful writing due to this problem.

Most of what you say is astonishingly precise and that makes me wonder the reason why I hadn’t looked at this in this light previously. Your article truly did turn the light on for me as far as this subject matter goes. Nonetheless there is one particular point I am not really too comfy with and while I make an effort to reconcile that with the actual main theme of your point, permit me see just what the rest of the visitors have to say.Well done.

The content is engaging and well-structured, keeping visitors interested.

The design and usability are top-notch, making everything flow smoothly.

Awsome article and straight to the point. I don’t know if this is truly the best place to ask but do you guys have any thoughts on where to employ some professional writers? Thanks in advance 🙂

This website is amazing, with a clean design and easy navigation.

The content is engaging and well-structured, keeping visitors interested.

This website is amazing, with a clean design and easy navigation.

AQUA SCULPT

I’m really impressed by the speed and responsiveness.

The layout is visually appealing and very functional.

Regards for this post, I am a big big fan of this site would like to go along updated.

I love how user-friendly and intuitive everything feels.

This site truly stands out as a great example of quality web design and performance.

This site truly stands out as a great example of quality web design and performance.

You really make it appear really easy together with your presentation however I find this topic to be actually one thing which I believe I’d never understand. It sort of feels too complicated and extremely extensive for me. I am having a look forward in your next submit, I?¦ll try to get the grasp of it!

This website is amazing, with a clean design and easy navigation.

The layout is visually appealing and very functional.

The design and usability are top-notch, making everything flow smoothly.

I went over this internet site and I think you have a lot of excellent info, saved to favorites (:.

I love how user-friendly and intuitive everything feels.

The content is well-organized and highly informative.

Thank you for the sensible critique. Me and my neighbor were just preparing to do some research on this. We got a grab a book from our area library but I think I learned more from this post. I am very glad to see such magnificent info being shared freely out there.

A perfect blend of aesthetics and functionality makes browsing a pleasure.

The design and usability are top-notch, making everything flow smoothly.

It provides an excellent user experience from start to finish.

I love how user-friendly and intuitive everything feels.

The content is engaging and well-structured, keeping visitors interested.

The layout is visually appealing and very functional.

A perfect blend of aesthetics and functionality makes browsing a pleasure.

It is truly a nice and helpful piece of information. I am satisfied that you shared this helpful info with us. Please keep us up to date like this. Thank you for sharing.

I do like the way you have framed this problem and it does indeed give us some fodder for thought. Nonetheless, coming from just what I have experienced, I simply just trust when other feed-back pack on that individuals stay on point and in no way get started upon a tirade associated with some other news du jour. Anyway, thank you for this outstanding point and even though I do not necessarily go along with this in totality, I value the perspective.

It provides an excellent user experience from start to finish.

A perfect blend of aesthetics and functionality makes browsing a pleasure.

This website is amazing, with a clean design and easy navigation.

This site truly stands out as a great example of quality web design and performance.

It provides an excellent user experience from start to finish.

I love how user-friendly and intuitive everything feels.

The layout is visually appealing and very functional.

Magnificent website. Plenty of useful info here. I am sending it to some pals ans also sharing in delicious. And of course, thanks for your sweat!

A perfect blend of aesthetics and functionality makes browsing a pleasure.

ICE HACK

Aumente o público das suas transmissões! Compre visualizações para live no YouTube e ganhe mais engajamento, credibilidade e alcance na plataforma.

The design and usability are top-notch, making everything flow smoothly.

You have brought up a very great points, thanks for the post.

The layout is visually appealing and very functional.

Thank you for sharing with us, I think this website really stands out : D.

It’s really a nice and useful piece of info. I’m glad that you simply shared this helpful info with us. Please keep us informed like this. Thank you for sharing.

The layout is visually appealing and very functional.

Hi! I know this is kind of off topic but I was wondering which blog platform are you using for this website? I’m getting fed up of WordPress because I’ve had problems with hackers and I’m looking at options for another platform. I would be fantastic if you could point me in the direction of a good platform.

I’m really impressed by the speed and responsiveness.

Very interesting topic, appreciate it for posting. “I am not an Athenian or a Greek, but a citizen of the world.” by Socrates.

Aw, this was a really nice post. In concept I want to put in writing like this moreover – taking time and actual effort to make a very good article… however what can I say… I procrastinate alot and not at all seem to get one thing done.

Your place is valueble for me. Thanks!…

This website is amazing, with a clean design and easy navigation.

hello!,I like your writing very much! share we communicate more about your article on AOL? I require a specialist on this area to solve my problem. May be that’s you! Looking forward to see you.

Great wordpress blog here.. It’s hard to find quality writing like yours these days. I really appreciate people like you! take care

The Natural Mounjaro Recipe is more than just a diet—it’s a sustainable and natural approach to weight management and overall health.

The design and usability are top-notch, making everything flow smoothly.

The Natural Mounjaro Recipe is more than just a diet—it’s a sustainable and natural approach to weight management and overall health.

The design and usability are top-notch, making everything flow smoothly.

It?¦s really a cool and helpful piece of info. I am happy that you just shared this helpful information with us. Please stay us informed like this. Thank you for sharing.

A perfect blend of aesthetics and functionality makes browsing a pleasure.

The Natural Mounjaro Recipe is more than just a diet—it’s a sustainable and natural approach to weight management and overall health.

The layout is visually appealing and very functional.

PrimeBiome is a dietary supplement designed to support gut health by promoting a balanced microbiome, enhancing digestion, and boosting overall well-being.

I like what you guys are up too. Such clever work and reporting! Keep up the superb works guys I¦ve incorporated you guys to my blogroll. I think it’ll improve the value of my site 🙂

I’m really impressed by the speed and responsiveness.

ProstaVive is a dietary supplement designed to promote prostate health, support urinary function, and improve overall well-being in men, especially as they age.

I have not checked in here for some time since I thought it was getting boring, but the last few posts are good quality so I guess I will add you back to my everyday bloglist. You deserve it my friend 🙂

The design and usability are top-notch, making everything flow smoothly.

A lot of of what you articulate is supprisingly precise and that makes me wonder why I hadn’t looked at this with this light previously. Your article really did turn the light on for me personally as far as this particular subject goes. Nonetheless at this time there is actually one point I am not necessarily too cozy with so while I try to reconcile that with the actual core theme of your position, allow me see just what all the rest of your readers have to say.Well done.

I’m really impressed by the speed and responsiveness.

It’s actually a nice and helpful piece of info. I’m glad that you just shared this helpful info with us. Please keep us informed like this. Thanks for sharing.

Great write-up, I am regular visitor of one¦s blog, maintain up the nice operate, and It’s going to be a regular visitor for a lengthy time.

I haven?¦t checked in here for a while because I thought it was getting boring, but the last few posts are great quality so I guess I will add you back to my daily bloglist. You deserve it my friend 🙂

Enjoyed examining this, very good stuff, thanks. “If it was an overnight success, it was one long, hard, sleepless night.” by Dicky Barrett.

Sweet internet site, super pattern, really clean and utilize friendly.

I really enjoy examining on this site, it holds great blog posts. “And all the winds go sighing, For sweet things dying.” by Christina Georgina Rossetti.

I have been browsing on-line more than three hours today, yet I by no means found any fascinating article like yours. It?¦s pretty worth sufficient for me. Personally, if all site owners and bloggers made good content as you probably did, the net will likely be a lot more useful than ever before.

Some truly great info , Gladiola I found this. “The outer conditions of a person’s life will always be found to reflect their inner beliefs.” by James Allen.

Japan is definitely on my bucket list! The mix of tradition and modernity is fascinating, and the food alone is enough reason to visit.

Thanks a bunch for sharing this with all of us you really know what you are talking about! Bookmarked. Please also visit my website =). We could have a link exchange arrangement between us!

I have read a few excellent stuff here. Definitely worth bookmarking for revisiting. I surprise how so much attempt you set to create such a wonderful informative website.

Consistency is key in fitness. You won’t see results overnight, but every workout counts. The small efforts add up over time and create real change.

You are a very bright person!

Thank you a bunch for sharing this with all of us you really realize what you’re talking about! Bookmarked. Please also visit my web site =). We will have a hyperlink alternate agreement among us!

Nothing beats homemade pasta. The texture and flavor are just on another level compared to store-bought versions. Cooking from scratch is truly an art.

Great items from you, man. I have keep in mind your stuff previous to and you are just too great. I actually like what you have got right here, really like what you’re stating and the way through which you are saying it. You make it enjoyable and you continue to take care of to keep it wise. I can’t wait to read much more from you. That is really a great web site.

What’s Taking place i’m new to this, I stumbled upon this I’ve found It absolutely helpful and it has aided me out loads. I hope to contribute & assist different users like its aided me. Great job.

Consistency is key in fitness. You won’t see results overnight, but every workout counts. The small efforts add up over time and create real change.

Watching a sunset over the ocean is one of the most peaceful experiences in life. Nature has a way of reminding us how small but connected we all are.

Hello! Someone in my Facebook group shared this website with us so I came to look it over. I’m definitely enjoying the information. I’m book-marking and will be tweeting this to my followers! Terrific blog and superb style and design.

Nothing beats homemade pasta. The texture and flavor are just on another level compared to store-bought versions. Cooking from scratch is truly an art.

You should take part in a contest for one of the best blogs on the web. I will recommend this site!

Keep up the fantastic work, I read few blog posts on this web site and I believe that your weblog is very interesting and holds bands of great information.

Fantastic beat ! I would like to apprentice while you amend your web site, how can i subscribe for a blog website? The account aided me a acceptable deal. I had been tiny bit acquainted of this your broadcast provided bright clear concept

Good – I should certainly pronounce, impressed with your web site. I had no trouble navigating through all tabs and related info ended up being truly simple to do to access. I recently found what I hoped for before you know it at all. Quite unusual. Is likely to appreciate it for those who add forums or anything, web site theme . a tones way for your customer to communicate. Nice task.

I found your blog web site on google and examine a few of your early posts. Continue to maintain up the superb operate. I simply additional up your RSS feed to my MSN News Reader. Searching for forward to reading more from you later on!…

Hey! This is kind of off topic but I need some help from an established blog. Is it very difficult to set up your own blog? I’m not very techincal but I can figure things out pretty fast. I’m thinking about making my own but I’m not sure where to begin. Do you have any ideas or suggestions? Appreciate it

Attractive portion of content. I simply stumbled upon your blog and in accession capital to assert that I acquire actually enjoyed account your blog posts. Any way I will be subscribing for your feeds or even I success you access persistently fast.

As I web-site possessor I believe the content material here is rattling wonderful , appreciate it for your hard work. You should keep it up forever! Good Luck.

Hey very nice blog!! Man .. Beautiful .. Amazing .. I’ll bookmark your site and take the feeds also…I’m happy to find numerous useful info here in the post, we need develop more strategies in this regard, thanks for sharing. . . . . .

I love it when people come together and share opinions, great blog, keep it up.

Mitolyn is a cutting-edge natural dietary supplement designed to support effective weight loss and improve overall wellness.

Thanks for helping out, superb info .

I appreciate, cause I found just what I was looking for. You’ve ended my four day long hunt! God Bless you man. Have a great day. Bye

Mitolyn is a cutting-edge natural dietary supplement designed to support effective weight loss and improve overall wellness.

I’ve read several good stuff here. Definitely worth bookmarking for revisiting. I wonder how much effort you put to make such a great informative website.

PrimeBiome is a dietary supplement designed to support gut health by promoting a balanced microbiome, enhancing digestion, and boosting overall well-being.

he blog was how do i say it… relevant, finally something that helped me. Thanks

What i do not realize is actually how you are not really much more well-liked than you might be right now. You’re so intelligent. You realize therefore considerably relating to this subject, produced me personally consider it from numerous varied angles. Its like women and men aren’t fascinated unless it is one thing to accomplish with Lady gaga! Your own stuffs excellent. Always maintain it up!

The Natural Mounjaro Recipe is more than just a diet—it’s a sustainable and natural approach to weight management and overall health.

Sweet blog! I found it while surfing around on Yahoo News. Do you have any suggestions on how to get listed in Yahoo News? I’ve been trying for a while but I never seem to get there! Appreciate it

پارتیشن سازه ، تولید کننده انواع پارتیشن اداری و سایر دکوراسیون اداری، با حدود سه دهه سابقه. با افتخار مجرئ انواع پروژهها در اکثریت شرکتها و ادارات. سفارش مستقیم از تولید کننده بدون واسطه

The Natural Mounjaro Recipe is more than just a diet—it’s a sustainable and natural approach to weight management and overall health.

Do you mind if I quote a few of your articles as long as I provide credit and sources back to your website? My blog site is in the very same area of interest as yours and my visitors would certainly benefit from a lot of the information you present here. Please let me know if this alright with you. Thank you!

Hi there just wanted to give you a quick heads up and let you know a few of the pictures aren’t loading properly. I’m not sure why but I think its a linking issue. I’ve tried it in two different browsers and both show the same results.

Mitolyn is a cutting-edge natural dietary supplement designed to support effective weight loss and improve overall wellness.

I’ve been browsing on-line greater than 3 hours these days, yet I never found any attention-grabbing article like yours. It is pretty value sufficient for me. In my view, if all site owners and bloggers made good content material as you probably did, the net will be a lot more helpful than ever before.

Some genuinely nice stuff on this website , I love it.

I really like what you guys are usually up too. This kind of clever work and reporting! Keep up the awesome works guys I’ve incorporated you guys to my blogroll.

I like this site very much, Its a really nice berth to read and incur info . “Misogynist A man who hates women as much as women hate one another.” by H.L. Mencken.

That is the best weblog for anyone who desires to seek out out about this topic. You notice a lot its nearly exhausting to argue with you (not that I truly would want…HaHa). You positively put a new spin on a topic thats been written about for years. Nice stuff, just nice!

ProDentim is a cutting-edge oral health supplement designed to improve dental and gum health by leveraging natural probiotics and nutrientes.

An impressive share, I just given this onto a colleague who was doing a little analysis on this. And he in fact bought me breakfast because I found it for him.. smile. So let me reword that: Thnx for the treat! But yeah Thnkx for spending the time to discuss this, I feel strongly about it and love reading more on this topic. If possible, as you become expertise, would you mind updating your blog with more details? It is highly helpful for me. Big thumb up for this blog post!

Thanx for the effort, keep up the good work Great work, I am going to start a small Blog Engine course work using your site I hope you enjoy blogging with the popular BlogEngine.net.Thethoughts you express are really awesome. Hope you will right some more posts.

I was recommended this blog by my cousin. I’m not sure whether this post is written by him as nobody else know such detailed about my trouble. You are amazing! Thanks!

I’m not that much of a online reader to be honest but your blogs really nice, keep it up! I’ll go ahead and bookmark your website to come back later on. Cheers

Some truly nice stuff on this site, I like it.

Howdy! I know this is kinda off topic but I’d figured I’d ask. Would you be interested in exchanging links or maybe guest authoring a blog article or vice-versa? My website goes over a lot of the same subjects as yours and I believe we could greatly benefit from each other. If you’re interested feel free to send me an email. I look forward to hearing from you! Fantastic blog by the way!

I went over this web site and I think you have a lot of wonderful information, saved to fav (:.

We stumbled over here coming from a different website and thought I might as well check things out. I like what I see so now i’m following you. Look forward to going over your web page for a second time.

Just desire to say your article is as surprising. The clearness for your post is just excellent and that i can think you are a professional in this subject. Fine with your permission allow me to snatch your feed to keep up to date with drawing close post. Thank you 1,000,000 and please carry on the gratifying work.

I conceive this internet site holds very good indited content content.

When I initially commented I clicked the “Notify me when new comments are added” checkbox and now each time a comment is added I get four e-mails with the same comment. Is there any way you can remove people from that service? Cheers!

I haven?¦t checked in here for some time because I thought it was getting boring, but the last few posts are good quality so I guess I?¦ll add you back to my everyday bloglist. You deserve it my friend 🙂

Hi there just wanted to give you a brief heads up and let you know a few of the pictures aren’t loading properly. I’m not sure why but I think its a linking issue. I’ve tried it in two different internet browsers and both show the same outcome.

Youre so cool! I dont suppose Ive read something like this before. So nice to search out someone with some authentic thoughts on this subject. realy thanks for beginning this up. this website is something that is needed on the web, someone with a bit originality. helpful job for bringing something new to the internet!

I loved as much as you will receive carried out right here. The sketch is attractive, your authored subject matter stylish. nonetheless, you command get bought an shakiness over that you wish be delivering the following. unwell unquestionably come more formerly again as exactly the same nearly very often inside case you shield this increase.

Helpful information. Fortunate me I found your site by chance, and I am shocked why this accident did not came about in advance! I bookmarked it.

Aw, this was a really nice post. In concept I want to put in writing like this additionally – taking time and precise effort to make an excellent article… but what can I say… I procrastinate alot and on no account appear to get something done.

I’m truly enjoying the design and layout of your website. It’s a very easy on the eyes which makes it much more enjoyable for me to come here and visit more often. Did you hire out a developer to create your theme? Great work!

I like this weblog very much, Its a really nice office to read and get info .

I intended to draft you that little bit of remark in order to say thanks a lot the moment again for your personal wonderful basics you’ve featured on this site. It was certainly extremely open-handed with you to grant publicly what exactly many of us might have offered as an e book to earn some dough for themselves, specifically considering the fact that you might well have done it if you decided. The pointers in addition acted like a fantastic way to be aware that someone else have the same passion just like my very own to see much more with regards to this matter. I’m sure there are millions of more pleasurable sessions in the future for individuals who read carefully your blog.

Hi my family member! I want to say that this post is amazing, great written and include almost all vital infos. I¦d like to look extra posts like this .

It is in point of fact a nice and helpful piece of information. I am glad that you just shared this helpful information with us. Please keep us up to date like this. Thanks for sharing.

My developer is trying to persuade me to move to .net from PHP. I have always disliked the idea because of the costs. But he’s tryiong none the less. I’ve been using Movable-type on a variety of websites for about a year and am worried about switching to another platform. I have heard good things about blogengine.net. Is there a way I can transfer all my wordpress posts into it? Any kind of help would be greatly appreciated!

Really wonderful visual appeal on this web site, I’d value it 10 10.

hey there and thank you on your information – I’ve definitely picked up something new from right here. I did then again expertise some technical points using this site, since I skilled to reload the website lots of occasions previous to I could get it to load properly. I were pondering in case your hosting is OK? No longer that I’m complaining, however slow loading cases occasions will often affect your placement in google and could injury your high quality score if ads and ***********|advertising|advertising|advertising and *********** with Adwords. Anyway I am adding this RSS to my e-mail and can glance out for much more of your respective fascinating content. Ensure that you replace this again soon..

Magnificent web site. A lot of helpful information here. I’m sending it to a few friends ans additionally sharing in delicious. And certainly, thank you in your effort!

15hx7n

I like the helpful info you provide in your articles. I will bookmark your blog and check again here frequently. I’m quite sure I’ll learn many new stuff right here! Best of luck for the next!

Even the gods, if they exist, must laugh from time to time. Perhaps what we call tragedy is merely comedy from a higher perspective, a joke we are too caught up in to understand. Maybe the wisest among us are not the ones who take life the most seriously, but those who can laugh at its absurdity and find joy even in the darkest moments.

Virtue, they say, lies in the middle, but who among us can truly say where the middle is? Is it a fixed point, or does it shift with time, perception, and context? Perhaps the middle is not a place but a way of moving, a constant balancing act between excess and deficiency. Maybe to be virtuous is not to reach the middle but to dance around it with grace.

Even the gods, if they exist, must laugh from time to time. Perhaps what we call tragedy is merely comedy from a higher perspective, a joke we are too caught up in to understand. Maybe the wisest among us are not the ones who take life the most seriously, but those who can laugh at its absurdity and find joy even in the darkest moments.

I think this is among the most vital information for me.

And i’m glad reading your article. But wanna remark on some general things,

The web site style is great, the articles is really great

: D. Good job, cheers

Thank you a lot for sharing this with all people you actually recognise what you are talking approximately! Bookmarked. Kindly also discuss with my web site =). We will have a hyperlink alternate agreement between us!

As a Newbie, I am constantly browsing online for articles that can help me. Thank you

It’s hard to find knowledgeable people on this topic, but you sound like you know what you’re talking about! Thanks

The essence of existence is like smoke, always shifting, always changing, yet somehow always present. It moves with the wind of thought, expanding and contracting, never quite settling but never truly disappearing. Perhaps to exist is simply to flow, to let oneself be carried by the great current of being without resistance.

I would like to thank you for the efforts you’ve put in writing this site. I am hoping the same high-grade blog post from you in the upcoming also. Actually your creative writing abilities has inspired me to get my own blog now. Actually the blogging is spreading its wings quickly. Your write up is a great example of it.

Friendship, some say, is a single soul residing in two bodies, but why limit it to two? What if friendship is more like a great, endless web, where each connection strengthens the whole? Maybe we are not separate beings at all, but parts of one vast consciousness, reaching out through the illusion of individuality to recognize itself in another.

Time is often called the soul of motion, the great measure of change, but what if it is merely an illusion? What if we are not moving forward but simply circling the same points, like the smoke from a burning fire, curling back onto itself, repeating patterns we fail to recognize? Maybe the past and future are just two sides of the same moment, and all we ever have is now.

I’ve been exploring for a bit for any high quality articles or blog posts on this sort of area . Exploring in Yahoo I at last stumbled upon this site. Reading this info So i am happy to convey that I’ve a very good uncanny feeling I discovered just what I needed. I most certainly will make sure to don’t forget this website and give it a look regularly.

Thank you for sharing with us, I conceive this website really stands out : D.

Hmm it looks like your website ate my first comment (it was extremely long) so I guess I’ll just sum it up what I wrote and say, I’m thoroughly enjoying your blog. I as well am an aspiring blog blogger but I’m still new to everything. Do you have any helpful hints for newbie blog writers? I’d genuinely appreciate it.

Even the gods, if they exist, must laugh from time to time. Perhaps what we call tragedy is merely comedy from a higher perspective, a joke we are too caught up in to understand. Maybe the wisest among us are not the ones who take life the most seriously, but those who can laugh at its absurdity and find joy even in the darkest moments.

I?¦ll immediately clutch your rss feed as I can’t find your e-mail subscription link or newsletter service. Do you have any? Please let me recognise so that I could subscribe. Thanks.

Even the gods, if they exist, must laugh from time to time. Perhaps what we call tragedy is merely comedy from a higher perspective, a joke we are too caught up in to understand. Maybe the wisest among us are not the ones who take life the most seriously, but those who can laugh at its absurdity and find joy even in the darkest moments.

I really like your blog.. very nice colors & theme. Did you create this website yourself or did you hire someone to do it

for you? Plz reply as I’m looking to construct my own blog and would like to find out where u got this from.

thank you

I have learn some just right stuff here. Definitely worth bookmarking for revisiting. I surprise how so much effort you set to create this sort of magnificent informative web site.

Thank you for the good writeup. It in truth was once a amusement account it. Look complex to more delivered agreeable from you! By the way, how can we keep in touch?

O Pix My Dollar é um aplicativo de microtarefas: você realiza atividades simples no celular e acumula recompensas, que podem ser convertidas em dinheiro.

I have been absent for some time, but now I remember why I used to love this site. Thank you, I?¦ll try and check back more frequently. How frequently you update your site?

Would you be fascinated by exchanging links?

O Pix My Dollar é um aplicativo de microtarefas: você realiza atividades simples no celular e acumula recompensas, que podem ser convertidas em dinheiro.

I am happy that I noticed this web blog, exactly the right info that I was searching for! .

Hey would you mind sharing which blog platform you’re working with? I’m planning to start my own blog soon but I’m having a hard time choosing between BlogEngine/Wordpress/B2evolution and Drupal. The reason I ask is because your design and style seems different then most blogs and I’m looking for something completely unique. P.S Sorry for being off-topic but I had to ask!

I conceive this internet site has got some real fantastic info for everyone. “Good advice is always certain to be ignored, but that’s no reason not to give it.” by Agatha Christie.

Hello There. I found your blog the usage of msn. This is a very neatly written article. I will be sure to bookmark it and return to learn more of your helpful information. Thank you for the post. I will definitely return.

O Pix My Dollar é um aplicativo de microtarefas: você realiza atividades simples no celular e acumula recompensas, que podem ser convertidas em dinheiro.

Really great information can be found on site.

Obrigado|Olá a todos, os conteúdos existentes nesta

Time is often called the soul of motion, the great measure of change, but what if it is merely an illusion? What if we are not moving forward but simply circling the same points, like the smoke from a burning fire, curling back onto itself, repeating patterns we fail to recognize? Maybe the past and future are just two sides of the same moment, and all we ever have is now.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Great ?V I should certainly pronounce, impressed with your website. I had no trouble navigating through all tabs as well as related info ended up being truly simple to do to access. I recently found what I hoped for before you know it at all. Quite unusual. Is likely to appreciate it for those who add forums or something, web site theme . a tones way for your customer to communicate. Excellent task..

I?¦ve recently started a website, the info you offer on this web site has helped me tremendously. Thank you for all of your time & work.

Wonderful paintings! That is the type of info that should be shared across the internet. Disgrace on the seek engines for no longer positioning this publish upper! Come on over and seek advice from my site . Thanks =)

Greetings! This is my first visit to your blog! We are a collection of volunteers and starting a new project in a community in the same niche. Your blog provided us useful information to work on. You have done a marvellous job!

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

Have you ever thought about creating an e-book or guest authoring on other websites? I have a blog centered on the same information you discuss and would really like to have you share some stories/information. I know my viewers would value your work. If you are even remotely interested, feel free to shoot me an e-mail.

I like the efforts you have put in this, regards for all the great blog posts.

Hey are using WordPress for your blog platform? I’m new to the blog world but I’m trying to get started and set up my own. Do you require any html coding expertise to make your own blog? Any help would be greatly appreciated!

I will right away seize your rss as I can not to find your e-mail subscription hyperlink or newsletter service. Do you have any? Kindly allow me recognise in order that I may just subscribe. Thanks.

Nice post. I learn something more challenging on different blogs everyday. It will always be stimulating to read content from other writers and practice a little something from their store. I’d prefer to use some with the content on my blog whether you don’t mind. Natually I’ll give you a link on your web blog. Thanks for sharing.

Wow that was odd. I just wrote an very long comment but after I clicked submit my comment didn’t appear. Grrrr… well I’m not writing all that over again. Anyhow, just wanted to say superb blog!

Hey very cool web site!! Man .. Beautiful .. Superb .. I’ll bookmark your website and take the feeds additionally?KI am satisfied to seek out so many helpful info here in the post, we need work out extra techniques on this regard, thank you for sharing. . . . . .

I visited various web pages but the audio quality for audio songs existing at this site is genuinely excellent.

Thank you for the sensible critique. Me and my neighbor were just preparing to do a little research on this. We got a grab a book from our area library but I think I learned more clear from this post. I am very glad to see such excellent information being shared freely out there.

Very efficiently written post. It will be helpful to anybody who usess it, including yours truly :). Keep doing what you are doing – for sure i will check out more posts.

I’m impressed, I need to say. Really hardly ever do I encounter a weblog that’s both educative and entertaining, and let me tell you, you have got hit the nail on the head. Your idea is outstanding; the issue is something that not sufficient persons are talking intelligently about. I am very blissful that I stumbled throughout this in my search for something relating to this.

I do consider all of the ideas you have introduced in your post. They’re really convincing and can definitely work. Still, the posts are very short for starters. Could you please extend them a little from subsequent time? Thanks for the post.

Fantastic website. A lot of useful information here. I am sending it to several friends ans additionally sharing in delicious. And naturally, thank you to your effort!

Hi, just required you to know I he added your site to my Google bookmarks due to your layout. But seriously, I believe your internet site has 1 in the freshest theme I??ve came across. It extremely helps make reading your blog significantly easier.

Some truly nice and utilitarian info on this site, likewise I think the style has got great features.

Greetings! Very helpful advice on this article! It is the little changes that make the biggest changes. Thanks a lot for sharing!

you are really a good webmaster. The website loading speed is amazing. It seems that you are doing any unique trick. Also, The contents are masterpiece. you have done a excellent job on this topic!

Very interesting points you have mentioned, appreciate it for putting up. “It’s the soul’s duty to be loyal to its own desires. It must abandon itself to its master passion.” by Rebecca West.

whoah this blog is fantastic i love reading your posts. Keep up the great work! You know, lots of people are searching around for this info, you can help them greatly.

WONDERFUL Post.thanks for share..more wait .. …

I like what you guys are up too. Such clever work and reporting! Keep up the superb works guys I’ve incorporated you guys to my blogroll. I think it will improve the value of my web site 🙂

I love your blog.. very nice colors & theme. Did you create this website yourself or did you hire someone to do it for you? Plz reply as I’m looking to construct my own blog and would like to find out where u got this from. thanks

I conceive this website contains some really good information for everyone : D.

You really make it seem really easy along with your presentation however I in finding this topic to be actually something that I believe I’d by no means understand. It sort of feels too complicated and extremely broad for me. I’m having a look ahead on your next put up, I¦ll attempt to get the hold of it!

you’re in point of fact a good webmaster. The web site loading speed is amazing. It kind of feels that you are doing any unique trick. Moreover, The contents are masterwork. you have done a excellent job in this matter!

F*ckin’ remarkable things here. I’m very glad to see your article. Thanks a lot and i’m looking forward to contact you. Will you please drop me a mail?

Oh my goodness! a tremendous article dude. Thank you Nonetheless I’m experiencing problem with ur rss . Don’t know why Unable to subscribe to it. Is there anybody getting identical rss downside? Anyone who is aware of kindly respond. Thnkx

Whats up! I just wish to give an enormous thumbs up for the nice information you’ve gotten here on this post. I will be coming again to your weblog for extra soon.

You made some good points there. I did a search on the subject matter and found most individuals will consent with your blog.

Rattling clean site, regards for this post.

Thanks for sharing excellent informations. Your website is so cool. I am impressed by the details that you?¦ve on this website. It reveals how nicely you perceive this subject. Bookmarked this website page, will come back for extra articles. You, my friend, ROCK! I found just the information I already searched all over the place and simply couldn’t come across. What a great website.

Can I just say what a relief to uncover somebody who

genuinely knows what they are discussing on the net.

You certainly realize how to bring an issue to light and

make it important. More people really need to look at this and understand

this side of the story. It’s surprising you’re not more popular given that

you surely possess the gift.

I think you have mentioned some very interesting details, regards for the post.

Howdy, i read your blog occasionally and i own a similar one and i was just curious if you get a lot of spam remarks? If so how do you reduce it, any plugin or anything you can suggest? I get so much lately it’s driving me crazy so any help is very much appreciated.

This web site is really a walk-through for all of the info you wanted about this and didn’t know who to ask. Glimpse here, and you’ll definitely discover it.

gul68b

What i don’t understood is if truth be told how you’re not really a lot more well-favored than you might be right now. You’re very intelligent. You recognize thus considerably on the subject of this topic, produced me individually believe it from a lot of numerous angles. Its like women and men are not interested unless it¦s something to accomplish with Lady gaga! Your individual stuffs outstanding. All the time take care of it up!

Great work! This is the type of information that should be shared around the internet. Shame on the search engines for not positioning this post higher! Come on over and visit my web site . Thanks =)

Dead written content, Really enjoyed studying.

nenarazili jste někdy na problémy s plagorismem nebo porušováním autorských práv? Moje webové stránky mají spoustu unikátního obsahu, který jsem vytvořil.

We are a group of volunteers and starting a brand new scheme in our community. Your site provided us with helpful information to paintings on. You have done an impressive activity and our whole neighborhood might be grateful to you.

I like what you guys are up too. Such intelligent work and reporting! Keep up the superb works guys I’ve incorporated you guys to my blogroll. I think it will improve the value of my website :).

It?¦s actually a great and helpful piece of information. I?¦m glad that you simply shared this useful info with us. Please keep us informed like this. Thank you for sharing.

I was suggested this web site by way of my cousin. I’m no longer positive whether this post is written by means of him as no one else recognise such designated approximately my trouble. You’re wonderful! Thank you!

Great web site. Lots of helpful info here. I¦m sending it to several friends ans also sharing in delicious. And naturally, thanks for your sweat!

I like the valuable info you provide in your articles. I’ll bookmark your weblog and check again here regularly. I’m quite sure I will learn plenty of new stuff right here! Good luck for the next!

fantastic points altogether, you just gained a new reader. What would you suggest about your post that you made some days ago? Any positive?

Great post. I was checking constantly this blog and I’m impressed! Very useful information particularly the last part 🙂 I care for such info a lot. I was looking for this particular info for a very long time. Thank you and best of luck.

Great site! I am loving it!! Will be back later to read some more. I am bookmarking your feeds also.

This really answered my problem, thank you!

Needed to draft you this very small word to finally say thanks a lot over again just for the awesome principles you’ve featured here. It is quite seriously open-handed with people like you to supply unhampered just what many individuals could have distributed as an e-book to help with making some money for their own end, and in particular considering that you could possibly have done it in case you wanted. The tricks also served to provide a great way to be aware that other people online have similar keenness just like my personal own to realize a lot more when considering this condition. Certainly there are a lot more pleasurable moments ahead for people who looked at your site.